IB Economics The Evolution of Money

Discover and learn how money evolved from silver shekels to Bitcoin, and why cryptocurrency might or might not be the future of finance. Master IB Economics

IB ECONOMICS HLIB ECONOMICS MACROECONOMICSIB ECONOMICSIB ECONOMICS SL

Lawrence Robert

5/16/20259 min read

From Silver Shekels to Bitcoin: Money in IB Economics

Target question:

What are the functions of money in IB Economics?

In prisons across the United States, packets of mackerel fillets are used as currency. And no, this is not a joke - they are being used as actual money. Inmates trade them for goods and services, lend them at interest, and quote prices in "macks." The reason is quite straightforward: mackerels last longer than most other commissary items, everyone values them, they can be divided into smaller units, and - the indispensable feature - the prison authorities can't "print" more of them. Mackerels satisfy, almost perfectly, the conditions that economists use to define money.

Which raises some real good questions from my students: what exactly makes something money, and does Bitcoin qualify? That's also what IB Economics Module 3 Macroeconomics wants you to be able to answer.

1. What Is Money? The IB Economics Definition

IB Economics definition - Money:

Any item or medium that is generally accepted as a means of payment for goods and services, and for the repayment of debts, within an economy.

IB Economics definition - Fiat Money:

Money that has no intrinsic value of its own - it is not backed by a physical commodity - but functions as money because a government has declared it legal tender and the public accepts it as such. All modern banknotes and coins are fiat money.

IB Economics definition - Commodity Money:

Money that has intrinsic value independent from its use as money. The item has value by itself - gold, silver, salt, animal furs - and also serves as a medium of exchange.

For most of human history, money was commodity money. A shekel in ancient Mesopotamia was one-third of an ounce of silver - the coin was worth something because the metal it was made from had market value. Gold and silver spread as monetary standards across ancient China, Egypt, India, and the Mediterranean because they were durable, portable, and relatively scarce.

In cold climates, animal furs served the same function; along inland trade routes, salt was used - hence the phrase "worth your salt," and the root of the word "salary." During the Cold War, behind the Iron Curtain, vodka served as an informal hard currency because it could be reliably exchanged for Western goods. So, commodities were different but the economic logic behind them was always the same.

Every episode of Pint-Sized links back to what matters most for your IB Economics course:

Understanding key IB Economics concepts

Applying them in real-world IB Economics contexts

Building IB Economics course confidence without drowning in dry theory.

Subscribe for free to exclusive episodes designed to boost your IB Economics grades and confidence

2. The Three Functions of Money

IB Economics defines money by what it does, not what it is made from. For something to qualify as money, it must perform three core functions:

Medium of Exchange

Money is accepted as payment for goods and services, eliminating the need for barter. Without a medium of exchange, trade requires a "double coincidence of wants" - the baker must want exactly what the farmer has, and vice versa, at exactly the same time. Having money removes totally this constraint.

Store of Value

Money retains its purchasing power over time, allowing economic agents to save and defer consumption. A farmer can sell the harvest now and spend the income generated months later. This function breaks down under high inflation - when prices rise rapidly, money loses value so quickly that people rush to spend it immediately rather than hold it.

Unit of Account

Money provides a common measure with which prices can be expressed and economic value compared. Without a unit of account, pricing would require quoting every good in terms of every other good - a market with 100 goods would need 4,950 exchange rates. Money reduces this to 100 prices.

Lawrence's exam note:

IB Economics Paper 1 questions on money may ask students to explain the functions and then evaluate whether a specific asset - cryptocurrency, gold, or even a commodity - fulfils them. Structure your response by working through each function systematically, with an example for each. Never mix the three functions - they are distinct, and failing to separate them is a common source of lost marks.

IB Economics - Syllabus and Programme Full Guide →

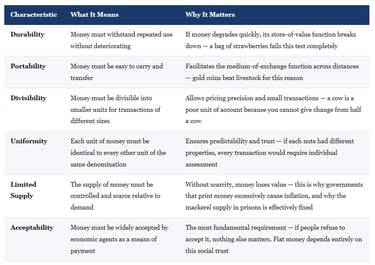

3. The Characteristics of Good Money

Beyond what money does, IB Economics also identifies what good money needs to be - the physical and institutional properties that allow money to perform its functions effectively in practice.

4. From Commodity Money to Fiat Money: The Historical Shift

The move from commodity money to paper fiat money in the nineteenth and twentieth centuries was one of the most significant institutional changes in economic history - and understanding this concept is relevant for your IB Economics course because it explains both how modern monetary policy works and why cryptocurrency emerged as an alternative.

Paper notes began replacing coins in widespread use around the 1800s. They were lighter, easier to produce, and simpler to carry in large quantities. The obvious problem was that a piece of paper has no intrinsic value - it is worth nothing except as money. To reassure the public that paper notes retained their store-of-value function, governments adopted the gold standard: promising to exchange any paper note for a fixed quantity of gold on demand. In the United States, the price of gold was fixed at $21 per ounce, and the government stood ready to respect that exchange.

The gold standard collapsed under pressure during the Great Depression (1933 in the US) and finally ended globally in 1971 when President Nixon ended the convertibility of the dollar to gold. From that point, the world moved entirely to fiat money - currency backed not by a physical commodity but by government decree and public trust. The pound in your pocket has value because everyone agrees it does, because the Bank of England manages its supply, and because the law requires it to be accepted as legal tender. That is, when you examine it closely, you will see a remarkable feat of collective social trust.

Related entry: For content of how central banks manage the money supply and set monetary policy, see:

IB Economics Monetary Policy Hub Page - Full Guide →

5. Does Cryptocurrency Qualify as Money? An IB Economics Evaluation

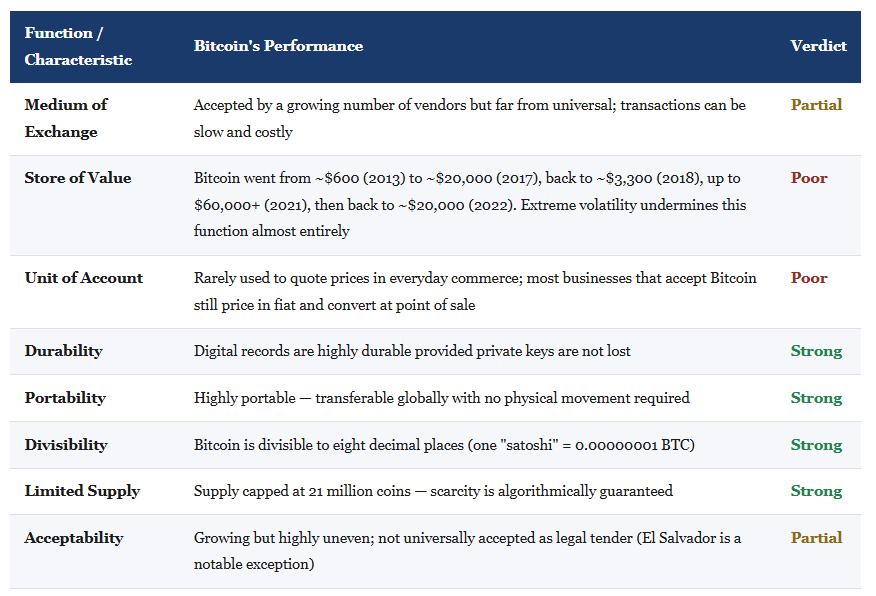

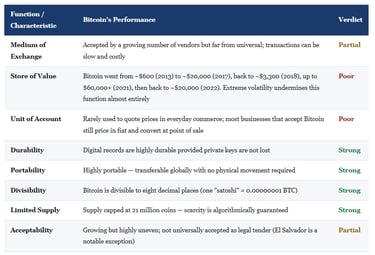

Bitcoin was invented in 2009 by the pseudonymous Satoshi Nakamoto - and it kicked off a genuine debate in economics about whether digital currencies can fulfil the functions and characteristics of money. To answer this in IB Economics terms, we need to evaluate cryptocurrency against each function and characteristic systematically, rather than simply describing price movements or investment benefits.

The IB Economics case for cryptocurrency is straightforward: it is decentralised (no government can inflate it away by printing more), its supply is algorithmically limited (Bitcoin is capped at 21 million coins), it is highly portable and divisible, and it is attractive in countries where central bank credibility is weak and domestic currencies have lost purchasing power rapidly - Argentina, Venezuela, and Zimbabwe being some good examples.

The case against Bitcoin is equally compelling:

The main contradiction is this: Bitcoin's most celebrated property - its extraordinary potential for appreciation - is what disqualifies it as effective money. When a Shiba Inu coin (created in 2020 as an internet meme) increases 330,000-fold in a single year, nobody spends it on everyday purchases. They hoard it, waiting to cash in later. And an asset that nobody spends is not functioning as a medium of exchange. The most dramatic example of this logic is the two pizzas purchased for 10,000 Bitcoin in 2010 - a transaction that, at Bitcoin's 2021 peak, represented a bill of over $600 million. The buyer was not irrational at the time; they simply treated Bitcoin as a currency rather than a speculative asset. Almost no one does that today.

Stable-coins - cryptocurrencies such as Tether that are pegged to the value of a traditional fiat currency and theoretically backed by equivalent reserves - attempt to solve the volatility problem. They aim to combine the technological advantages of cryptocurrency (speed, decentralisation, digital transfer) with the price stability required for the store-of-value and unit-of-account functions. Whether they succeed depends on the credibility of their reserve backing - a concern that several high-profile stable-coin collapses have increased.

Central Bank Digital Currencies (CBDCs) HL

The response of central banks to the rise of cryptocurrency has been to explore their own digital currencies. A Central Bank Digital Currency (CBDC) would combine the technological infrastructure of cryptocurrency with the institutional backing and stability of traditional fiat money. China has already piloted a digital yuan; the Bank of England has explored a "digital pound." This is relevant to a great extent in IB Economics: a CBDC is fiat money in digital form, issued and controlled by a central bank, and therefore subject to standard monetary policy tools. It is not a decentralised cryptocurrency - it is rather the opposite.

Lawrence's exam notes:

If asked in Paper 1 or IB Economics Paper 2 to evaluate whether cryptocurrency functions as money, the IB Economics approach is: define money and its three functions, define the relevant characteristics, evaluate cryptocurrency against each criterion systematically using specific examples, and reach a reasoned conclusion. The conclusion consistent with the evidence currently available is that current major cryptocurrencies (Bitcoin, Ethereum) function better as speculative assets than as money - because price volatility undermines the store-of-value and unit-of-account functions. A balanced response acknowledges their potential role in economies with severely dysfunctional fiat currencies.

IB Economics Diagrams Programme, What's included:

200+ exam-ready diagrams covering the entire IB Economics syllabus

Video for every diagram showing you exactly how each model looks

Image version perfect for modelling diagrams in you essays, presentations, and your IA

Detailed written explanations of the IB Economics theory behind each diagram

Both SL and HL IB Economics diagrams clearly labelled and organised by topic

Real IB Economics exam application showing how to use diagrams effectively in Paper 1 and Paper 2

Frequently Asked Questions: Money in IB Economics

Q: What are the three functions of money in IB Economics?

The three functions of money in IB Economics are: (1) medium of exchange - money is accepted as payment for goods and services, eliminating the need for barter and a double coincidence of wants; (2) store of value - money retains its purchasing power over time, allowing economic agents to save and defer consumption; and (3) unit of account - money provides a common measure in which prices can be expressed and economic values compared. For money to function effectively, all three functions must be performed reliably. High inflation destroys the store-of-value function; extreme volatility, as seen in cryptocurrency markets, undermines both the store of value and unit of account functions.

Q: What are the characteristics of good money in IB Economics?

IB Economics identifies six key characteristics of good money: durability (money must withstand repeated use without deteriorating), portability (it must be easy to carry and transfer), divisibility (it must be divisible into smaller units for transactions of different sizes), uniformity (each unit must be identical to every other unit of the same denomination), limited supply (scarcity relative to demand is required to maintain value), and acceptability (money must be widely accepted as a means of payment). Fiat money - modern banknotes and coins - meets all six characteristics, which is why it has become the dominant form of money globally.

Q: What is the difference between commodity money and fiat money in IB Economics?

Commodity money has intrinsic value independent of its monetary use - gold, silver, salt, and animal furs are historical examples. The item is worth something even if it stops being used as money. Fiat money, by contrast, has no intrinsic value - it is declared legal tender by a government and functions as money purely because the public accepts it as such and the law requires it to be accepted in settlement of debts. All modern national currencies are fiat money. The shift from commodity to fiat money began in the nineteenth century with paper notes backed by gold (the gold standard) and was completed in 1971 when the US ended gold convertibility of the dollar.

Q: Does Bitcoin function as money in IB Economics terms?

Evaluated against the IB Economics criteria, Bitcoin performs strongly on some characteristics (portability, divisibility, limited supply, durability) but poorly on the functions most essential to money. Its extreme price volatility - moving from roughly $600 in 2013 to $60,000 in 2021 and back to $20,000 in 2022 - severely undermines its store-of-value function and makes it impractical as a unit of account. Its use as a medium of exchange remains limited. In practice, Bitcoin and most major cryptocurrencies function more as speculative assets than as money, though they may serve a monetary role in economies where domestic fiat currencies have lost credibility through hyperinflation.

Q: Why does high inflation damage the functions of money in IB Economics?

High inflation erodes the purchasing power of money over time, directly undermining the store-of-value function - money held today buys less tomorrow. When inflation is severe, economic agents rush to spend money as quickly as possible rather than hold it, which also weakens the medium-of-exchange function as people lose confidence in the currency. In hyperinflationary environments - Zimbabwe in the 2000s, Weimar Germany in the 1920s - domestic currencies have effectively stopped functioning as money entirely, with economic agents switching to foreign currencies, barter, or commodity substitutes. This is why central banks target low, stable inflation rather than zero inflation or deflation.

Explore Topics:

IB Economics your IB Economics daily guide

IB Economics Macroeconomics access Monetary Policy here as well as the rest of the module

IB Economics Diagrams Check Unit 22 for All Monetary Policy diagrams with explanations

IB Economics Activity book Module 3 Macroeconomics Unit 3.15 for Monetary Policy exam practice, activities, model answers and IB Economics Marking schemes

IB Economics Monetary Policy (Tools and Overview) - essential reading

IB Economics Inflation - essential learning when discussing the value of money and purchasing power

IB Economics Fiscal Policy for exploring in depth the contrast between Monetary Policy and Fiscal Policy strengths and limitations of both.

IB economics Calculations Book make sure you check unit 21 for Monetary Policy calculations exercises, IB model answers, and IB marking schemes

Read Next: IB Economics Corporate and Government Bonds

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form