IB Economics Corporate and Government Bonds

Discover why bonds are basically fancy IOUs, and how their prices affect almost everything from mortgages to student loans. Essential IB Economics content.

IB ECONOMICS HLIB ECONOMICS MACROECONOMICSIB ECONOMICSIB ECONOMICS SL

Lawrence Robert

5/17/202511 min read

Bonds Explained: Government and Corporate IOUs in IB Economics

Target Question:

What is the relationship between bond prices and bond yields in IB Economics?

If you've ever lent a tenner to a friend and got a promise of £12 back at the end of term you've already experienced the basic structure of a bond. When governments need to build hospitals, or corporations want to expand factories, they rarely have the cash sitting around. So they do what your friend did: they borrow, they promise to repay, and they offer something to the lender in return for the wait. The difference is that governments borrow billions, the repayment terms are written into legal contracts, and the whole process is traded on global financial markets that influence interest rates in your economy.

In the IB Economics syllabus you will not find a dedicated chapter on government and corporate bonds. But understanding bonds is essential background knowledge for several main IB Economics topics: government borrowing and fiscal policy, monetary policy transmission, and - for HL students - financial markets. When a news headline says "UK gilt yields have risen sharply" or "the Fed's decision pushed bond prices down," you need to know what that means and why it may be relevant for the macroeconomic topics you are being examined on.

Useful content connected to bonds:

Fiscal Policy (Module 3): Governments issue bonds to finance budget deficits - understanding bonds explains how government borrowing actually works in practice.

Monetary Policy (Module 3): Central banks conduct open market operations by buying and selling government bonds, which directly influences bond yields and broader interest rates throughout the economy.

Exchange Rates (HL Module 4): Bond markets are a core component of the global financial system. HL students need to understand how bond markets allocate capital and transmit financial conditions internationally. When a country's bond yields rise, its currency generally appreciates because higher returns attract foreign investors who must buy that currency to invest.

Complete IB Economics Activity Book:

52 Complete Units including Government and Corporate Bonds

Every unit from all four modules: Every topic. Every concept. Every theory. Nothing left out.

900+ Practice Activities

Complete IB Standard Model Answers

IB Standard Marking Schemes

Exam Practice Questions

Always Updated The Living Resource Advantage

1. What Is a Bond? The Core Concept

IB Economics definition - Bond:

A financial instrument (a debt security) through which a borrower - typically a government or corporation - raises money by promising to make specified future payments to the bondholder. The borrower is the bond issuer; the lender is the bondholder.

IB Economics definition - Face Value (Par Value):

The amount the bond issuer promises to repay to the bondholder at maturity. Typically set at a round number - £1,000, $10,000 - when the bond is first issued.

IB Economics definition - Maturity Date:

The future date on which the issuer repays the face value to the bondholder. Bond maturities range from a few months (Treasury bills) to thirty years or more (long-dated government bonds).

IB Economics definition - Coupon Payment:

A regular interest payment made by the bond issuer to the bondholder, typically every six months or annually. Calculated as the face value multiplied by the coupon rate.

A bond differs from a standard bank loan in an important structural way. When you take out a student loan, you specify how much you want to borrow, and the lender tells you what the repayments will be. With a bond, the borrower specifies what they are willing to pay in the future, and the market determines how much investors are willing to lend today in exchange for that promise. The bond is then tradeable - it can be bought and sold between investors on secondary markets before of its maturity date.

Government bonds go by different names in different countries: they are called gilts in the UK, Treasuries in the United States, Bunds in Germany, and JGBs (Japanese Government Bonds) in Japan. When a government runs a budget deficit - spending more than it collects in tax revenue - it typically finances the gap by issuing bonds. Understanding this mechanism is directly relevant to IB Economics fiscal policy analysis.

Related entry: For full coverage of how governments use borrowing as part of fiscal policy, see:

IB Economics Fiscal Policy - Full Guide →

2. Zero-Coupon Bonds: The Simplest Bonds

To understand how bond pricing works, start with the simplest type: a zero-coupon bond. This is similar to one of your friends who never buys rounds at the pub all evening but promises to cover everyone's kebabs at the end of the night. You get nothing until the very end - just one single payment at maturity.

Suppose the US government issues a $10,000 zero-coupon bond maturing in ten years. This means:

You hand over some amount of money today

The government pays you exactly $10,000 in ten years

No payments whatsoever in between

So, How much would you pay for that $10,000 promise today? Clearly not $10,000 - because $10,000 today is worth more than $10,000 in ten years. You could invest $10,000 today and earn returns over the decade. The bond is only attractive if you can buy it at a discount.

IB Economics definition - Yield to Maturity (Bond Yield):

The effective annual interest rate earned by a bondholder who purchases the bond at the current market price and holds it until maturity. It is the return that makes the present value of the bond's future payments equal to its current price.

If you buy that $10,000 zero-coupon ten-year bond for $6,000, your yield to maturity is 5.24% - that is the annual return on your $6,000 investment that produces $10,000 after ten years. If you paid $8,000, your yield falls to 2.26% - you paid more for the same future payment, so your effective return is lower.

3. The Truth: Bond Prices and Yields Move in Opposite Directions

This inverse relationship is the single most important thing to understand about bond markets, and the concept that is basic for IB Economics exam contexts.

↓ Bond Price Falls → Bond Yield Rises ↑

↑ Bond Price Rises → Bond Yield Falls ↓

The future payment is fixed. The cheaper you buy it, the higher your return. The more you pay, the lower your effective return.

Why is this relevant beyond bond markets? government bond yields - particularly US Treasury yields and UK gilt yields - serve as the benchmark interest rate from which virtually all other borrowing costs in the economy are derived.

When government bond yields rise, mortgage rates rise, corporate borrowing costs rise, and the cost of financing government debt rises. When central banks conduct open market operations - buying or selling government bonds to influence the money supply - they are directly manipulating bond prices and therefore yields, which then ripple through every interest rate in the economy.

IB Economics connection to monetary policy:

When a central bank wants to reduce interest rates, it buys government bonds on the open market. This increased demand pushes bond prices up - and because of the inverse relationship, bond yields fall. Lower yields feed through to lower mortgage rates, lower corporate borrowing costs, and cheaper government financing. This is the transmission mechanism of monetary policy in practice. HL students need to understand this chain explicitly; SL students benefit from knowing it as context for why central bank decisions affect the broader economy.

Related entry: For full coverage of how central banks use interest rates and open market operations, see:

IB Economics Monetary Policy - Full Guide →

Every episode of Pint-Sized links back to what matters most for your IB Economics course:

Understanding key IB Economics concepts

Applying them in real-world IB Economics contexts

Building IB Economics course confidence without drowning in dry theory.

Subscribe for free to exclusive episodes designed to boost your IB Economics grades and confidence

4. What Influences Bond Prices? The RIAS Framework

Four factors determine how much an investor is willing to pay for a bond today - and therefore determine its yield. The mnemonic RIAS covers all four:

R-Risk

Would you rather lend to the UK government or to a start-up your cousin launched last week? The higher the perceived risk that the borrower will default - fail to make promised payments - the less investors will pay for the bond, pushing yields higher. Risk is the most important driver of yield differences between borrowers.

I-Inflation

If inflation is expected to be high over the bond's life, the fixed future payment will be worth less in real terms. Investors demand compensation by paying less for the bond today - pushing yields higher. This is why bond markets react quickly to inflation data and central bank inflation forecasts.

A-Alternatives

If other investments - equities, savings accounts, property - offer higher returns, bonds look less attractive. Investors demand better yields to stay in bonds, pushing prices down. When the stock market booms, government bond prices often fall as investors move toward equities.

S-Impatience (Time Preference)

Economic agents generally prefer money now to money later - economists call this positive time preference. The further away the maturity date, the more compensation investors demand for waiting, all else equal. This is why long-dated bonds typically offer higher yields than short-dated bonds from the same issuer.

IB Economics - Syllabus and Programme Full Guide →

5. Risk Premiums: Why You Are Not the Government

IB Economics definition - Risk Premium:

The additional interest rate charged to a borrower above the risk-free rate (typically the government bond yield) to compensate lenders for the higher probability that the borrower may default.

IB Economics definition - Default:

The failure of a bond issuer to make promised payments - either coupon payments or the face value repayment at maturity.

Let's imagine that ten-year UK government gilts yield 4%. When you apply for a ten-year student loan, the bank looks at you and reaches a negative conclusion: you are a considerably a higher credit risk than His Majesty's Treasury. So they add a risk premium - say 2.25 percentage points - and charge you 6.25% for lending you this money.

Your friend with three credit cards over the limit gets assessed as an even higher risk, so their risk premium is larger - perhaps 3.5 percentage points, meaning they pay 7.5%. If gilt yields fall to 2%, and assuming risk premiums stay constant, your rate falls to 4.25% and your friend's to 5.5%. This is the mechanism through which central bank policy - which influences government bond yields - transmits to household and corporate borrowing costs across the entire economy.

Risk premiums can also change independently of government yields. After the 2008 subprime mortgage crisis, banks sharply raised risk premiums on home loans to borrowers with moderate credit scores, even as central banks cut base rates - a real-world example of risk premiums moving against the direction of monetary policy.

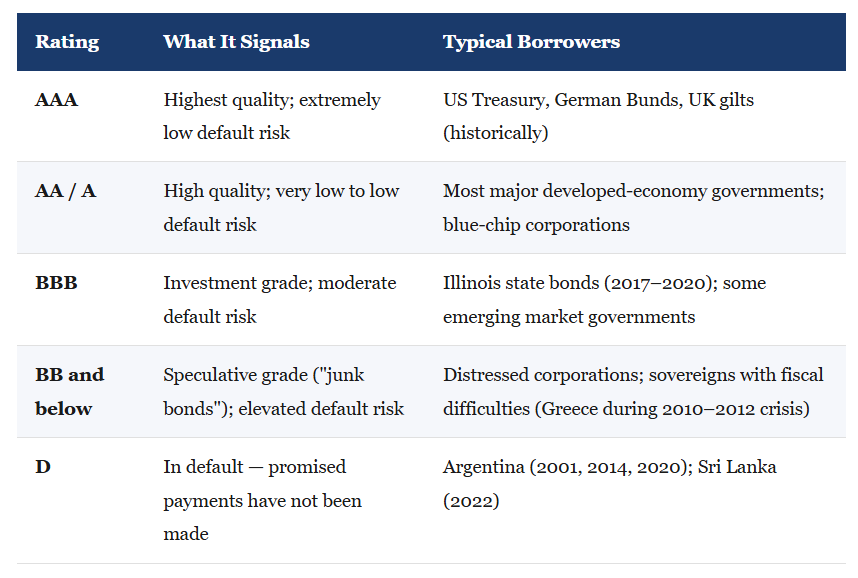

6. Credit Ratings: The Bond Market's Report Card

Just as your predicted grades determined which universities would consider your application, credit ratings determine how cheaply governments and corporations can borrow on bond markets. Ratings agencies - Moody's, Standard and Poor's (S&P), and Fitch - assess the likelihood that a bond issuer will default, and summarise their assessment in a letter rating.

The higher a borrower's rating, the lower the risk premium investors demand, and therefore the lower the interest rate required to attract buyers. This has direct implications for fiscal policy: a government whose credit rating is downgraded faces immediately higher borrowing costs, which constrains its ability to fund public services, infrastructure, and welfare programmes through deficit spending. Greece's experience during the sovereign debt crisis - when its bonds were repeatedly downgraded to junk status, making it impossible to borrow affordably on markets - is the perfect illustration of how bond market confidence can constrain government policy choices.

IB Economics Exam Application:

Bonds may not have their own unit in the IB Economics syllabus, but they appear regularly as stimulus/reference material in IB Economics Paper 2 data response questions and as context in IB Economics Paper 1 evaluation. When you see references to "rising gilt yields," "government borrowing costs," "central bank bond purchases," or "sovereign debt risk," bonds are the analytical framework behind those phrases. A student who can explain why rising bond yields increase the cost of fiscal stimulus - and why central bank bond purchases lower mortgage rates - demonstrates the kind of critical thinking and understanding that separates a grade 6 from a 7.

IB Economics Diagrams Programme, What's included:

200+ exam-ready diagrams covering the entire IB Economics syllabus

Video for every diagram showing you exactly how each model looks

Image version perfect for modelling diagrams in you essays, presentations, and your IA

Detailed written explanations of the IB Economics theory behind each diagram

Both SL and HL IB Economics diagrams clearly labelled and organised by topic

Real IB Economics exam application showing how to use diagrams effectively in Paper 1 and Paper 2

Frequently Asked Questions: Bonds in IB Economics

Q: What is the relationship between bond prices and bond yields in IB Economics?

Bond prices and bond yields move in opposite directions - this inverse relationship is one of the most important concepts in financial economics. When a bond's price falls, its yield (effective interest rate) rises, because the fixed future payment now represents a higher return relative to the lower price paid. When the price rises, the yield falls. This relationship matters in IB Economics because government bond yields serve as benchmark interest rates from which mortgage rates, corporate borrowing costs, and other market interest rates are derived. Central bank open market operations work by buying or selling bonds to push yields up or down, transmitting monetary policy through the entire economy.

Q: What is a government bond and how does it connect to fiscal policy in IB Economics?

A government bond is a debt security issued by a government to raise money, typically to finance a budget deficit. The government promises to repay the face value on a specified maturity date and usually pays regular coupon (interest) payments in the interim. In IB Economics, government bonds are directly relevant to fiscal policy: when a government runs a deficit and cannot cover its spending through taxation alone, it finances the gap by issuing bonds. The rate of interest it must pay - the bond yield - is determined by market confidence in the government's creditworthiness. A downgraded credit rating raises yields and increases the cost of financing deficit spending.

Q: What is a risk premium in bond markets and why does it matter for IB Economics?

A risk premium is the additional interest rate a borrower must pay above the risk-free rate - usually the government bond yield - to compensate lenders for the higher probability of default. In IB Economics, risk premiums explain why different borrowers face different interest rates even when monetary policy is identical for all. A household, a corporation, and a government all borrow at different rates because their perceived default risk differs. Central bank policy moves the baseline yield, but risk premiums - which reflect lender confidence in each borrower - move independently, which is why monetary policy does not affect all borrowers equally.

Q: What are credit ratings and why do they matter for government borrowing in IB Economics?

Credit ratings are assessments issued by ratings agencies (Moody's, S&P, Fitch) that summarise the probability that a bond issuer will default on their promised payments. Ratings range from AAA (lowest risk, lowest borrowing cost) to D (already in default). For IB Economics, credit ratings matter because they directly influence the interest rate a government must pay to borrow. A downgrade raises the risk premium investors demand, increasing borrowing costs and constraining fiscal policy options. Greece's sovereign debt crisis (2010–2012) illustrates this: successive downgrades to junk status made it impossible for Greece to borrow on markets at sustainable rates, ultimately requiring international bailouts.

Q: How do central bank bond purchases affect interest rates in IB Economics?

When a central bank buys government bonds on the open market - a policy known as quantitative easing or open market operations - increased demand pushes bond prices up. By the inverse price-yield relationship, rising bond prices mean falling yields. Lower government bond yields reduce the benchmark rate from which all other borrowing costs are derived, leading to lower mortgage rates, lower corporate borrowing costs, and cheaper government financing. This is the transmission mechanism through which central banks influence economic activity beyond simply setting a policy interest rate. IB Economics HL students need to understand this chain explicitly; SL students benefit from understanding it as context for how monetary policy affects aggregate demand.

Stay well,

Explore Topics:

IB Economics your IB Economics daily guide

IB Economics Macroeconomics access Monetary Policy and Bond related content here as well as the rest of module 3.

IB Economics Diagrams Check Unit 22 for All Monetary Policy diagrams with explanations

IB Economics Government Intervention as governments use Bonds as a tool to finance a lot of their interventions.

IB Economics Activity book Module 3 Macroeconomics Unit 3.15 for Monetary Policy and Bond exam practice, activities, model answers and IB Economics Marking schemes

IB Economics Monetary Policy (Tools and Overview) - essential reading

IB Economics Consequences of Inflation as this content has a direct relationship with Bonds

IB Economics Inflation - essential learning when discussing Bonds

IB Economics Fiscal Policy for exploring in depth the contrast between Monetary Policy and Fiscal Policy and their relationship to Bonds.

IB economics Calculations Book make sure you check unit 21 for Monetary Policy calculations exercises, IB model answers, and IB marking schemes

Read Next: IB Economics Interest Rates

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form