IB Economics Interest Rates Explained

Understand how interest rates work through British examples! Perfect for IB Economics students - explained using student loans, and your future housing dreams

IB ECONOMICS HLIB ECONOMICS MACROECONOMICSIB ECONOMICSIB ECONOMICS SL

Lawrence Robert

5/18/202511 min read

Interest Rates in IB Economics: The Price of Borrowing Time

Target Question:

How do interest rate changes affect the economy in IB Economics?

In March 2020, the Bank of England cut its Bank Rate from 0.75% to 0.1% in an emergency decision - the lowest level in the institution's 325-year history. By August 2023, it had risen to 5.25%, the highest in fifteen years, before a gradual cutting cycle brought it to 3.75% by early 2026. Your are probably asking yourselves, so what? Well, each percentage point shift reshapes the borrowing costs of millions of households, the investment decisions of thousands of firms, and the fiscal room available to the UK government. Understanding why interest rates behave this way, and how interest rate changes impact an economy, is essential background knowledge for several of the most examined topics in IB Economics module 3 macroeconomics.

IB Economics Related Content:

Monetary Policy (Module 3): Interest rates are the primary tool of monetary policy. The Bank of England's Monetary Policy Committee sets the Bank Rate to influence inflation, output, and employment.

Aggregate Demand (Module 3): Interest rate changes affect consumption (C) and investment (I) - two of the four components of AD. A rate cut increases both, shifting the AD curve rightward.

Exchange Rates (Module 4): Interest rate differentials drive international capital flows, which directly influence the exchange rate and therefore export competitiveness.

Nominal vs Real Interest Rates (IB Economics HL Module 3): HL students must distinguish between nominal and real interest rates and understand how inflation affects the true cost of borrowing.

1. What Is an Interest Rate? The IB Economics Definition

IB Economics definition - Interest Rate:

The price of borrowing money, expressed as a percentage of the amount borrowed per year. From the lender's perspective, it is the return earned for supplying funds. From the borrower's perspective, it is the cost paid for access to funds.

IB Economics definition - Nominal Interest Rate:

The stated interest rate on a loan or deposit, unadjusted for inflation. If a bank pays 4% on a savings account, 4% is the nominal rate.

IB Economics definition - Real Interest Rate:

The nominal interest rate adjusted for inflation. It represents the true purchasing power gain (or cost) of lending (or borrowing). Calculated using the Fisher equation:

Real interest rate ≈ Nominal interest rate − Inflation rate.

The difference between nominal / real interest rate is extremely relevant in practice. If a bank offers a savings account at 4% nominal interest but annual inflation is running at 3.3% - as it was in the UK in early 2026 - the real interest rate is only approximately 0.7%. The saver is barely growing their purchasing power in real terms. At the same time, when inflation exceeded the Bank Rate during 2022–2023, real interest rates were briefly negative - meaning borrowers were effectively being paid in real terms to take out loans, while savers were losing real value despite earning positive nominal returns.

IB Economics HL note:

HL Paper 1 questions frequently ask students to distinguish between nominal and real interest rates and to explain why the real rate - not the nominal rate - is the relevant rate for investment and saving decisions. An investor deciding whether to build a new factory cares about the real cost of borrowing, not the nominal rate. If inflation rises unexpectedly after a fixed-rate loan is taken out, the real borrowing cost falls even though the nominal rate is unchanged. Always apply the Fisher equation when asked to evaluate the true impact of interest rate changes.

(1 + i) = (1 + r) (1 + π)

i = Nominal interest rate (the stated rate on a loan or investment)

r = Real interest rate (the purchasing power of the interest earned)

π = Inflation rate

2. The Time Value of Money: Why £1,000 Today Is Worth More Than £1,000 Tomorrow

The logic behind interest rates is simple: money available today is worth more than the same amount in the future, because today's money can be invested or lent to generate a return. An interest rate is the price that summarises this difference - it is what a borrower must pay to access funds now rather than later, and what a lender receives for postponing their own spending.

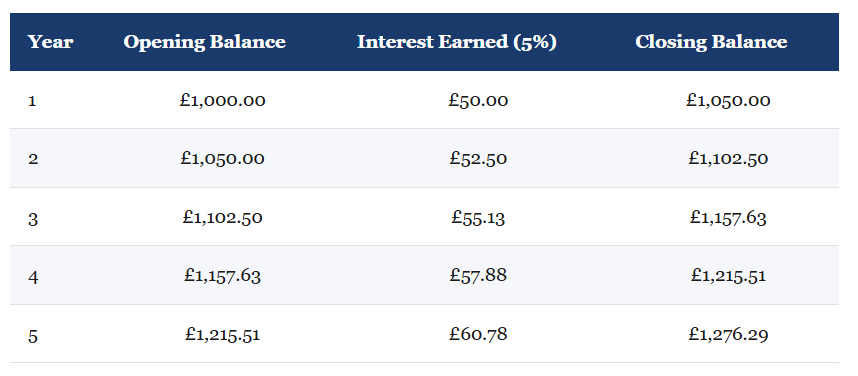

Suppose you deposit £1,000 in a savings account earning 5% annual interest, compounded annually:

After five years, your £1,000 has become £1,276.29 - a gain of £276.29 without any additional saving. This compounding effect is why higher interest rates increase the incentive to save and reduce the incentive to borrow: the future reward for saving (and the future cost of borrowing) grows with each percentage point the interest rate rises.

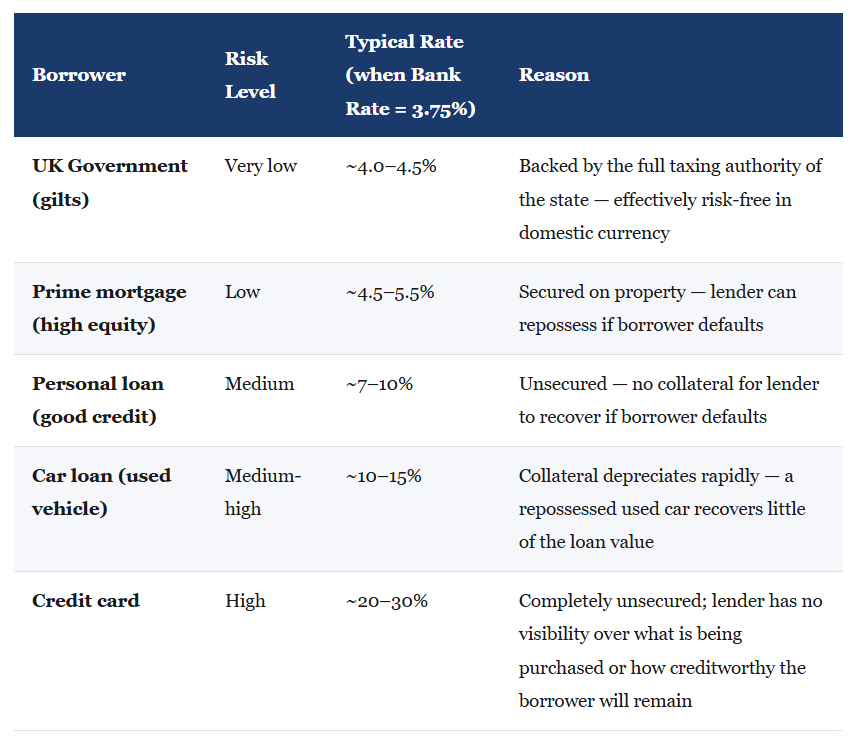

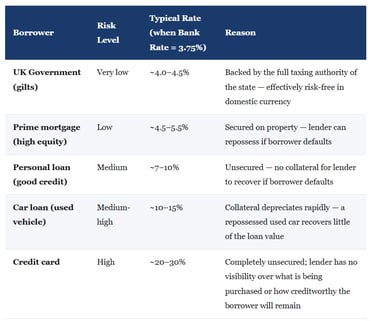

3. Risk and Interest Rates: Why All Rates Are Not Equal

Not all borrowers pay the same interest rate - and the explanation lies in the risk factor. Every lender assesses how likely they are to be repaid and charges a higher rate to compensate for higher default risk. This additional charge above the risk-free rate is the risk premium.

The Bank Rate set by the Bank of England establishes the foundation. When it moves, every rate above it typically shifts by a similar amount - because the risk premium for each type of borrower remains broadly constant while the baseline moves up or down. This is the transmission mechanism through which monetary policy affects the entire economy.

IB Economics Related entry: For the role of bond yields in this risk premium structure and how they connect to government borrowing costs, see:

IB Economics Corporate and Government Bonds - Full Guide →

4. The Bank of England and the Bank Rate

IB Economics definition - Bank Rate (Base Rate):

The interest rate set by the Bank of England's Monetary Policy Committee (MPC) at which commercial banks can borrow from the Bank of England overnight. It is the most important interest rate in the UK economy, serving as the floor from which all other lending and saving rates are derived.

The Bank Rate is the Bank of England's primary monetary policy tool. The MPC meets every six weeks to decide whether to raise it, cut it, or hold it unchanged, based on its assessment of inflation, output, and employment. As of May 2026, the Bank Rate stands at 3.75%, held at its April 2026 meeting with the MPC voting eight to one in favour of holding the rate. UK CPI inflation was 3.3% in the twelve months to March 2026 - above the Bank's 2% target - which is why rate cuts have been cautious and gradual despite the cutting cycle that began in August 2024.

The Bank Rate is basically the UK economy's financial thermostat. When the economy is overheating - inflation rising, spending running ahead of productive capacity - the Bank raises the rate to cool things down. When the economy is sluggish - output falling, unemployment rising, deflation risk emerging - it cuts the rate to encourage spending and investment.

5. How Interest Rate Changes Impact the Economy

A change in the Bank Rate does not transform the economy instantly - it works through a series of channels that together constitute the monetary policy transmission mechanism. Understanding this chain is essential for IB Economics monetary policy analysis:

①

Bank Rate changes → Commercial banks adjust their lending and saving rates. A rate cut reduces the cost of mortgages, business loans, and consumer credit. Rising rates increases them.

②

Borrowing costs change → Household consumption is affected. Cheaper credit encourages consumer spending on durable goods (cars, appliances, home improvements) and housing. Higher credit costs reduce discretionary spending as mortgage repayments absorb more household income.

③

Investment changes → Lower interest rates reduce the cost of capital for firms, making previously marginal investment projects possible. Higher rates raise the hurdle rate for investment, suppressing capital expenditure. This affects the investment (I) component of aggregate demand directly.

④

Aggregate demand shifts → Changes in consumption and investment shift the AD curve. A rate cut → AD shifts right → real output rises, price level rises. A rate rise → AD shifts left → output falls, inflation pressure eases.

⑤

Exchange rate adjusts → Higher UK interest rates attract foreign capital seeking better returns, increasing demand for pounds. The pound appreciates, making exports more expensive and imports cheaper - which itself reduces inflationary pressure but harms export competitiveness.

Lawrence's notes:

The transmission mechanism takes time. The Bank of England estimates that interest rate changes take 18–24 months to exert their full effect on inflation and output. This time lag is one of the most important limitations of monetary policy and is a high-value evaluation point in both IB Economics Paper 1 and IB Economics Paper 2. A government facing a recession cannot simply cut rates today and expect recovery by next quarter - and this lag creates the risk of policy error, where a rate change designed for today's conditions lands in a very different economic environment.

IB Economics - Syllabus and Programme Full Guide →

6. Interest Rates and Exchange Rates

The exchange rate channel deserves specific attention because it connects IB Economics Module 3 Macroeconomics (monetary policy) directly to Module 4 (the global economy and international trade).

When the Bank of England raises the Bank Rate relative to rates in other countries, UK financial assets offer higher returns than equivalent foreign assets. This attracts international capital flows into the UK - foreign investors sell their currencies to buy pounds and invest in UK bonds or savings accounts. Increased demand for pounds pushes the pound's exchange rate upwards.

A stronger pound has two effects that work in opposite directions for the economy: it reduces import prices (which helps bring inflation down, supporting the Bank's objective) but makes UK exports more expensive in foreign markets (which reduces export demand and can harm UK manufacturers and services exporters). This trade-off is a typical evaluation point in IB Economics exchange rate and monetary policy questions.

IB Economics Related content: For full coverage of how exchange rates affect trade and the current account, see:

IB Economics Exchange Rates - Full Guide →

7. Winners and Losers from Interest Rate Changes

Similar to inflation, interest rate changes redistribute real income between different groups - and the IB Economics key concept of equity applies directly here.

Winners When Rates Rise

Savers and depositors. Higher rates mean greater nominal returns on cash savings and fixed-income investments. Pensioners and retirees relying on savings income benefit directly.

Lenders and creditors. Banks and financial institutions earn higher margins on their loan books. New loans are issued at higher rates, improving lenders profitability.

Those on fixed-rate mortgages already locked in. Existing fixed-rate borrowers are insulated from rate rises until their deal ends and then they must re-mortgage.

Losers When Rates Rise

Mortgage holders on variable or tracker rates. Monthly repayments increase immediately as the Bank Rate rises. The 2022–2023 rate cycle added hundreds of pounds per month to typical UK mortgage costs.

Businesses with variable-rate borrowing. Firms carrying debt at floating rates face higher interest costs, squeezing profit margins and suppressing investment.

Government. Higher rates increase the cost of servicing national debt, reducing fiscal space for public spending. The UK's debt interest bill rose sharply during the 2022–2023 tightening cycle.

First-time buyers. Higher mortgage rates reduce affordability, pricing more buyers out of the housing market.

IB Economics Real-life example:

When the Bank of England raised its Bank Rate from 0.1% in December 2021 to 5.25% by August 2023 - fourteen consecutive increases - approximately 1.8 million UK fixed-rate mortgages came up for renewal in 2024 alone. Homeowners who had locked in at rates below 2% faced re-mortgaging to rates above 4.5%, adding over £300 per month to typical repayments. This real-world squeeze on household disposable income illustrates how monetary policy transmits to consumption and aggregate demand - and why rate changes have distributional consequences as well as macroeconomic ones.

IB Economics Diagrams Course

Every monetary policy diagram - AD/AS expansionary and contractionary policy, money market, and Phillips Curve monetary policy application - fully labelled with video support.

✔ Expansionary and contractionary monetary policy AD/AS diagrams

✔ Money market interest rate diagrams

✔ Phillips Curve and monetary policy connection

✔ 200+ diagrams covering the full syllabus · Both SL and HL labelled

Frequently Asked Questions: Interest Rates in IB Economics

Q: How do interest rate changes affect the economy in IB Economics?

In IB Economics, interest rate changes work through the monetary policy transmission mechanism across several channels. A rate cut by the central bank reduces borrowing costs for households and firms, stimulating consumption and investment - both components of aggregate demand - and shifting the AD curve rightward. Lower rates also tend to weaken the exchange rate (as capital flows seek higher returns elsewhere), making exports more competitive but raising import prices. A rate rise operates in reverse: reducing consumption and investment, shifting AD leftward, easing inflation pressure, and strengthening the exchange rate. The full effects take 18–24 months to materialise, which is a key limitation of monetary policy.

Q: What is the difference between nominal and real interest rates in IB Economics?

The nominal interest rate is the stated rate on a loan or deposit, unadjusted for inflation. The real interest rate adjusts for inflation and represents the true purchasing power cost of borrowing (or return on lending). The Fisher equation states: real interest rate ≈ nominal interest rate − inflation rate. For example, if the Bank Rate is 3.75% and CPI inflation is 3.3%, the real interest rate is approximately 0.45%. The distinction is significant in IB Economics because investment and saving decisions are driven by real rates, not nominal rates - and when inflation exceeds the nominal rate, real interest rates become negative, which dramatically changes economic incentives.

Q: What is the Bank Rate and how does it relate to monetary policy in IB Economics?

The Bank Rate is the interest rate set by the Bank of England's Monetary Policy Committee (MPC) at which commercial banks can borrow from the Bank of England overnight. It is the UK's primary monetary policy instrument. When the MPC raises the Bank Rate, borrowing costs throughout the economy increase, reducing consumption and investment and helping to bring down inflation. When it cuts the rate, borrowing becomes cheaper, stimulating spending and output. As of May 2026, the Bank Rate stands at 3.75%, held amid above-target inflation of 3.3%. The Bank Rate serves as the foundation of the entire UK interest rate structure - all commercial lending and saving rates are set relative to it.

Q: Why do different borrowers pay different interest rates in IB Economics?

Different borrowers pay different interest rates because lenders charge a risk premium on top of the risk-free rate (typically the government bond yield) to compensate for the probability of default. The higher the lender's assessment of default risk, the larger the risk premium and the higher the interest rate charged. A government borrowing in its own currency carries near-zero default risk and pays the lowest rates; a household with a poor credit score borrowing unsecured on a credit card carries high default risk and pays rates of 20–30%. Between these extremes, mortgage rates are lower than personal loan rates because the property provides collateral - the lender can recover value by repossessing the asset if the borrower defaults.

Q: How do interest rates affect exchange rates in IB Economics?

Higher domestic interest rates attract foreign capital flows into a country, as investors seek better returns on bonds, savings accounts, and other financial assets. This increased demand for the domestic currency causes it to appreciate. A stronger exchange rate makes exports more expensive in foreign markets (reducing export competitiveness) but makes imports cheaper (helping to reduce domestic inflation). This is why interest rate increases can have a disinflationary effect through two channels simultaneously: suppressing domestic demand via higher borrowing costs, and reducing import prices through currency appreciation. The exchange rate channel is one of the most important - and most examined - aspects of the monetary policy transmission mechanism in IB Economics.

Explore Topics:

IB Economics your IB Economics daily guide

IB Economics Macroeconomics access Monetary Policy, Interest Rates theory here as well as the rest of module 3

IB Economics The Business Cycle - useful information when discussing deflationary and inflationary gaps

IB Economics Consequences of Inflation useful content for assessing inflation's impact on the economy

IB Economics Diagrams Check Unit 22 for All Monetary Policy diagrams with explanations

IB Economics Bonds Explained for relevant content on bonds functioning and their relationship with interest rates

IB Economics Activity book Module 3 Macroeconomics Unit 3.15 for Monetary Policy and Interest Rates related questions exam practice, activities, model answers and IB Economics Marking schemes

IB Economics Monetary Policy (Tools and Overview) - essential reading

IB Economics Inflation - essential learning when discussing real vs nominal rates and inflationary gaps

IB Economics Fiscal Policy for exploring in depth the contrast between Monetary Policy and Fiscal Policy strengths and limitations of both.

IB Economics Aggregate Demand content directly related to interest rates

IB economics Calculations Book make sure you check unit 21 for Monetary Policy and Interest Rates calculations exercises, IB model answers, and IB marking schemes

Read Next: IB Economics The Minimum Wage Explained

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form