IB Monetary Policy

Target Question:

What is monetary policy in IB Economics and how does it work?

Everything you need to understand, analyse, and evaluate monetary policy for your IB Economics course - tools, transmission mechanisms, effectiveness, limitations, and real-world applications.

Full monetary policy activity practice breakdown, exam practice, model answers and evaluation tools are available exclusively in the IB Economics Activity Book.

What Is Monetary Policy?

Monetary policy refers to the actions taken by a country's central bank to influence the money supply, credit conditions, and interest rates in order to achieve macroeconomic objectives - primarily price stability (low, stable inflation), but also supporting economic growth and employment.

It is one of the two main tools of macroeconomic management alongside fiscal policy. The key institutional distinction: in most modern economies, monetary policy is controlled by an independent central bank rather than elected government - insulating interest rate decisions from short-term political pressures.

IB Economics definition:

Monetary policy is the use of interest rates, money supply, and related instruments by a central bank to influence aggregate demand and achieve macroeconomic objectives, primarily price stability. Expansionary monetary policy lowers interest rates to stimulate demand; contractionary monetary policy raises interest rates to reduce inflationary pressure.

Expansionary monetary policy - lower interest rates, increased money supply - shifts the AD curve rightward, stimulating growth and reducing unemployment. Used during recessions or periods of deficient demand. Source: IB Economics Diagrams

Contractionary monetary policy - higher interest rates, reduced money supply - shifts the AD curve leftward, reducing inflationary pressure. Used when the economy is overheating or inflation exceeds the target. Source: IB Economics Diagrams

Central Bank Tools

Interest Rate Policy

The primary tool of modern monetary policy. The central bank sets a policy rate - the rate at which it lends to commercial banks overnight. Changes in the policy rate feed through to commercial lending rates, mortgage rates, and savings rates across the economy.

Raising rates - increases borrowing costs, reduces consumer spending and business investment, cools aggregate demand, and reduces inflationary pressure

Lowering rates - reduces borrowing costs, stimulates spending and investment, increases aggregate demand, and supports growth

Most major central banks operate under inflation targeting - an explicit commitment to maintaining inflation at a specified rate (typically 2%). The target provides an anchor for inflation expectations, enhancing policy credibility and reducing the risk of self-fulfilling inflationary spirals.

Open Market Operations

The central bank buys or sells government securities in financial markets to influence the money supply and short-term interest rates. Buying securities injects money into the banking system (expansionary); selling withdraws money (contractionary). Open market operations are the day-to-day mechanism through which central banks implement their target interest rate.

Reserve Requirements

The minimum proportion of deposits that commercial banks must hold as reserves, rather than lend out. Raising reserve requirements reduces banks' capacity to create credit; lowering them increases it. In practice, reserve requirements are rarely used as an active policy tool in modern advanced economies - interest rate policy is more flexible and precise.

Forward Guidance

Central bank communication about future policy intentions as a tool in its own right. By credibly signalling that rates will remain low for an extended period, the central bank can influence long-term interest rates and economic decisions today, even without changing the current rate. This is particularly important when short-term rates are near zero and conventional policy space is limited.

Quantitative Easing (QE)

When conventional interest rate policy reaches its limits - when rates are at or near zero - central banks can use QE: large-scale purchases of financial assets (government bonds, mortgage-backed securities) to inject money directly into the financial system and push down long-term interest rates.

QE aims to:

Lower long-term borrowing costs beyond what short-term rate cuts can achieve

Raise asset prices, generating wealth effects that support spending

Weaken the currency, boosting export competitiveness

QE was deployed extensively following the 2008 financial crisis and again during the COVID-19 pandemic. The Federal Reserve's balance sheet grew from approximately $900 billion before 2008 to over $8 trillion at its peak - a scale unprecedented in peacetime.

The Transmission Mechanism

How monetary policy reaches the real economy is one of the most important concepts in IB Economics macroeconomics. The transmission mechanism operates through several channels:

Interest rate channel - the most direct route. Lower policy rates reduce mortgage costs, consumer credit rates, and business borrowing costs, stimulating spending and investment. Higher rates do the reverse.

Credit channel - lower rates increase banks' willingness to lend and borrowers' willingness to borrow, expanding credit availability. Higher rates tighten credit conditions, reducing lending and spending.

Asset price channel - lower rates push up equity and property prices (by making other assets less attractive and reducing discount rates). Higher asset prices generate wealth effects, increasing consumer spending.

Exchange rate channel - lower domestic interest rates reduce capital inflows (foreign investors earn less), weakening the exchange rate. A weaker currency makes exports cheaper and imports more expensive, boosting net exports and aggregate demand. Higher rates attract capital inflows, strengthen the currency, and reduce export competitiveness.

Expectations channel - credible monetary policy shapes and modifies inflation and growth expectations. If households and firms believe the central bank will achieve its inflation target, they set wages and prices accordingly - making the target self-fulfilling and reducing the output cost of disinflation.

Central Bank Independence

Central bank independence - the separation of monetary policy decisions from direct political control - is one of the most important features of modern monetary frameworks.

The case for independence: elected politicians face incentives to stimulate the economy before elections and tolerate above-target inflation, creating an inflationary bias. Independent central banks, insulated from electoral pressures, can credibly commit to price stability - anchoring expectations and reducing the inflation premium in long-term interest rates.

The case against full independence: monetary policy decisions have significant distributional consequences - higher interest rates hurt borrowers and benefit savers; QE inflates asset prices and benefits the wealthy. Democratic accountability arguments suggest such decisions should not be entirely removed from elected oversight.

In practice, most central banks are operationally independent (free to set rates to achieve the target) but goal-dependent (the inflation target itself is set by government). The Bank of England, Federal Reserve, and ECB all operate within this framework.

Limitations of Monetary Policy

Strong IB Economics monetary policy evaluation and critical thinking must include its limitations.

Time lags - monetary policy works with significant delays. The full effect of an interest rate change on inflation and output typically takes 12-24 months to materialise. This makes it difficult to calibrate policy with precision - by the time a rate rise reduces inflation, economic conditions may have changed substantially.

The zero lower bound (ZLB) - conventional interest rate policy cannot push rates significantly below zero (there are limits to how far negative rates can go before cash hoarding undermines the banking system). When rates hit zero during a deep recession, conventional monetary policy is exhausted - the liquidity trap. QE was developed as a response to this constraint.

Effectiveness depends on bank lending behaviour - if commercial banks are reluctant to lend (as after the 2008 financial crisis, when banks were rebuilding capital), lower policy rates may not translate into lower lending rates or expanded credit. Policy can lead to a liquidity trap where monetary stimulus fails to stimulate spending.

Cannot address supply-side inflation - monetary policy manages demand. It cannot reduce cost-push inflation caused by oil price shocks or supply chain disruptions without accepting a significant output sacrifice. The 1970s stagflation demonstrated this: raising rates to fight supply-shock inflation worsened unemployment without addressing the underlying cause.

Distributional effects - interest rate changes affect different groups differently. Higher rates hurt variable-rate mortgage holders, small businesses dependent on credit, and developing countries with dollar-dependent debt, while benefiting savers and creditors. QE inflates asset prices, disproportionately benefiting wealthier households with larger financial asset holdings.

Open economy constraints - in small open economies, the exchange rate channel can dominate, creating complications. A rate rise attracts capital inflows and strengthens the currency - potentially worsening the current account even as domestic demand falls.

IB Economics - Syllabus and Programme Full Guide →

Real-Life Applications

The Volcker disinflation (1979-82) - Federal Reserve Chair Paul Volcker raised US interest rates to 21% to break entrenched double-digit inflation. The result was a deep recession but a decisive defeat of inflationary expectations - the SRPC shifted downward as the Fed's credibility was established. It remains the definitive example of using contractionary monetary policy to anchor expectations, and directly illustrates both the effectiveness and the output cost of aggressive rate rises.

Post-2008 QE - with rates at zero after the global financial crisis, major central banks deployed QE at unprecedented scale. The policy prevented a deeper depression and kept long-term rates low, but generated concerns about asset price inflation, inequality effects, and the challenge of eventual normalisation.

2021-2024 inflation cycle - the post-pandemic inflation surge (peaking above 10% in the UK and US) encouraged the most aggressive monetary tightening since the Volcker era. Central banks raised rates sharply from near-zero, demonstrating both the continuing relevance of conventional rate policy and the challenges of calibrating it when inflation arises from supply-side shocks rather than demand excess.

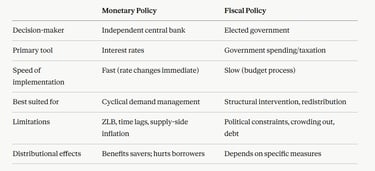

Monetary vs Fiscal Policy: Key Comparison

IB Economics frequently asks students to compare monetary and fiscal policy. The key distinctions:

In practice, effective macroeconomic management requires coordination between the two - as demonstrated during the COVID-19 response, where massive fiscal stimulus was complemented by near-zero rates and QE to keep borrowing costs low.

Monetary Policy in the IB Economics Exam

Monetary policy is examined across all papers:

IB Economics Paper 1 - essay questions ask students to explain monetary policy tools with AD/AS diagrams, evaluate expansionary vs contractionary stances, compare monetary with fiscal policy, or assess the case for central bank independence. The 15-mark response requires genuine evaluation: time lags, ZLB constraints, supply-side limitations, and distributional effects alongside the potential effectiveness.

IB Economics Paper 2 - data response questions present interest rate or inflation data and ask students to apply theory, interpret trends, or evaluate policy decisions.

IB Economics Paper 3 HL - extended questions may integrate monetary policy with the Phillips Curve, exchange rates, or development economics.

Most common exam mistakes: explaining only one direction of monetary policy (expansionary or contractionary) without the other; not using AD/AS diagrams; evaluating effectiveness without acknowledging time lags and the ZLB; failing to compare monetary and fiscal policy when the question invites it.

IB Economics Fiscal Policy - Full Guide →

IB Economics Phillips Curve - Full Guide →

IB Economics Exchange Rates - Full Guide →

IB Economics Inflation - Full Guide →

IB Economics Diagrams Course

Every monetary policy diagram - AD/AS expansionary and contractionary policy, money market, and Phillips Curve monetary policy application - fully labelled with video support.

✔ Expansionary and contractionary monetary policy AD/AS diagrams

✔ Money market interest rate diagrams

✔ Phillips Curve and monetary policy connection

✔ 200+ diagrams covering the full syllabus · Both SL and HL labelled

Frequently Asked Questions: Monetary Policy in IB Economics

What is monetary policy in IB Economics? Monetary policy is the use of interest rates and related instruments by an independent central bank to influence aggregate demand and achieve macroeconomic objectives - primarily price stability (low, stable inflation). Expansionary monetary policy lowers interest rates to stimulate demand during recessions; contractionary monetary policy raises rates to reduce inflationary pressure when the economy overheats.

What is the transmission mechanism of monetary policy? The transmission mechanism describes how central bank rate changes affect the real economy. The main channels are: the interest rate channel (lower rates reduce borrowing costs, stimulating spending); the credit channel (lower rates expand bank lending); the asset price channel (lower rates raise equity and property prices, generating wealth effects); the exchange rate channel (lower rates weaken the currency, boosting exports); and the expectations channel (credible policy anchors inflation expectations, making the target self-fulfilling).

What is quantitative easing and when is it used? Quantitative easing (QE) is a monetary policy tool used when conventional interest rate policy is exhausted - typically when rates are at or near zero. The central bank purchases large quantities of financial assets (government bonds, mortgage securities) to inject money into the financial system, push down long-term interest rates, and stimulate lending and spending. It was deployed extensively after the 2008 financial crisis and during the COVID-19 pandemic.

What are the main limitations of monetary policy? Key limitations include: time lags (12-24 months for full effects); the zero lower bound (conventional rates cannot go significantly below zero, creating a liquidity trap); ineffectiveness against supply-side inflation (raising rates during a supply shock worsens output without addressing the cause); dependence on bank lending behaviour (banks may not pass on rate cuts); and distributional effects (rate changes benefit savers but hurt borrowers; QE inflates asset prices, favouring the wealthy).

Why is central bank independence important in IB Economics? Central bank independence removes monetary policy from direct political control, eliminating the inflationary bias that is often generated when elected politicians face incentives to stimulate the economy before elections. Independent central banks can credibly commit to price stability - anchoring inflation expectations and reducing the inflation premium in long-term interest rates. The counter-argument is that distributional consequences of monetary decisions warrant democratic oversight - most modern frameworks compromise with operational independence combined with government-set inflation targets.

This hub is updated regularly to reflect current IB Economics syllabus requirements and monetary policy developments.

Explore Topics:

IB Economics your IB Economics daily guide

IB Economics Macroeconomics access Monetary Policy here as well as the rest of the module

IB Economics Diagrams Check Unit 22 for All Monetary Policy diagrams with explanations

IB Economics Inflation - essential learning when discussing real vs nominal rates and inflationary gaps

IB Economics Activity book Module 3 Macroeconomics Unit 3.15 for Monetary Policy exam practice, activities, model answers and IB Economics Marking schemes

IB Economics The Business Cycle Hub is directly related to Monetary Policy and recessions, revise this theory

IB Economics Fiscal Policy for exploring in depth the contrast between Monetary Policy and Fiscal Policy.

IB economics Calculations Book make sure you check unit 21 for Monetary Policy calculations exercises, IB model answers, and IB marking schemes

Read Next: IB Economics Price Ceiling and Price Floor

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form