IB Economics the Business Cycle

Master the business cycle for IB Economics! Learn the 5 stages with real UK examples, Netflix & gaming industry case studies. Student-friendly guide.

IB ECONOMICS HLIB ECONOMICS SLIB ECONOMICSIB ECONOMICS MACROECONOMICSIB ECONOMICS INTRODUCTION

Lawrence Robert

7/27/202512 min read

The Business Cycle as a Policy Analysis Tool: How to Use It in IB Economics Essays

Target Question:

How does the business cycle affect macroeconomic policy in IB Economics?

Most if not all of my IB Economics students can describe the business cycle. But only some can use it analytically to determine which policy response is appropriate to solve specific cycles, which economic problems are temporary and which are permanent, and which indicators signal where an economy currently sits. That analytical gap is where usually IB Economics Paper 1 marks are won and lost.

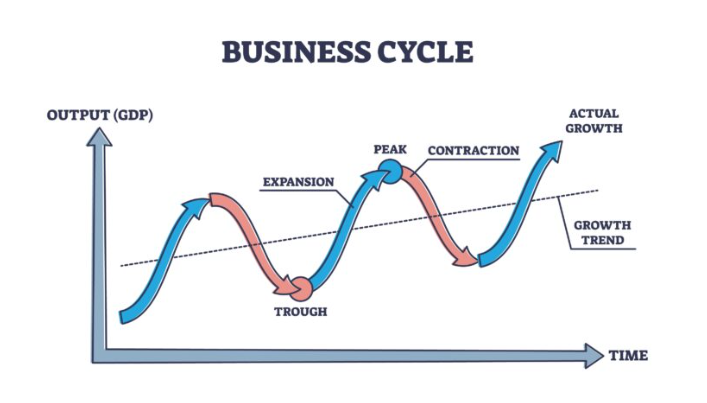

This entry is not a description of the business cycle phases - you can find that content in our IB Economics business cycle entry. It is a guide to apply successfully the business cycle framework as an analytical tool in IB macroeconomics: making the cyclical vs structural distinction, reading economic indicators correctly, evaluating policy effectiveness at different points in the cycle, and avoiding the most common errors in business cycle essay responses.

For extended content and explanations of why recessions occur, see our IB Economics recessions guide entry. For government policy responses, see the countercyclical fiscal policy entry.

The Most Important Distinction: Cyclical vs Structural

The most valuable analytical skill provided by the business cycle framework is the ability to differentiate between cyclical and structural problems. This distinction helps identify the appropriate policy intervention. Not being able to identify these issues can result in proposing ineffective policies and lower exam scores.

IB Economics Definition - Cyclical vs Structural Unemployment:

Cyclical unemployment is caused by deficient aggregate demand during a recession. It falls automatically as the economy recovers and rises toward potential output - it is, by definition, temporary. Structural unemployment reflects a persistent mismatch between workers' skills and employers' needs, arising from technological change or sectoral shifts. It persists regardless of where the economy is in the cycle and cannot be resolved by demand stimulus alone.

For example, in a recessionary economy with an unemployment rate of 8%, it’s important to analyse the what that figure is made of. You should consider how much of the 8% is cyclical and how much is structural. Given that the pre-recession unemployment rate stood at 5%, which IB economic theory indicates is the natural rate of unemployment (consisting of frictional and structural unemployment), we can deduce that approximately 3 percentage points are cyclical, added from the recession. The remaining 5 percentage points represent structural or frictional unemployment. This natural rate of unemployment exists regardless of economic conditions.

Once we have carried out this analysis the policy implications vary significantly. Demand-side stimulus, such as fiscal expansion or monetary easing, can effectively tackle the cyclical aspect by increasing aggregate demand, narrowing the output gap, and bringing employment back to pre-recession levels. However, it cannot put an end to the structural issues. For instance, no amount of demand stimulus will retrain a coal miner so he can work in software engineering or address the geographical mismatch between job locations and worker residences. To tackle these challenges, we need to implement supply-side interventions, including retraining programmes, education reform, and housing policies that enhance labour mobility.

An IB Economics response that suggests fiscal stimulus as the sole solution to unemployment, without recognising that part of the unemployment problem is structural, will lose marks, even if the multiplier and a correct explanation are included. In order to analyse the business cycle framework properly we need to show the examiner the ability to provide this analysis and highlight this context before proposing any policy recommendations.

IB Economics Definition - Cyclical vs Structural Budget Deficit:

A cyclical budget deficit is caused by the automatic fall in tax revenues and rise in transfer payments during a recession. It narrows automatically during recovery without requiring policy action. A structural deficit persists even when the economy operates at potential output - it reflects a fundamental imbalance between government spending commitments and revenue capacity that will not resolve through economic recovery alone.

The same cyclical vs structural concept distinction applies to government budget deficits. During the 2008-09 recession, the UK government borrowing rose sharply - from roughly 3% of GDP pre-crisis to over 10% at its peak. Part of this downturn was cyclical: tax revenues fell and benefit payments rose automatically as unemployment increased. However, this aspect would recover automatically later on as the economy grew. At the same time, part was structural: the pre-crisis fiscal position had been built on revenue from a financial sector whose profitability collapsed permanently. This part would not recover automatically and required deliberate fiscal adjustment.

When it comes to evaluating IB Economics questions you should include this as part of your answer. A government facing only a cyclical deficit does not necessarily need to implement austerity - the deficit will close as the economy recovers. A government with a large structural deficit faces a more fundamental challenge that requires either spending reduction or revenue increases even at full employment. Combining the two in your answer - treating all deficit reduction as equally urgent, or treating all deficits as self-correcting - produces poor policy evaluation and poor analysis.

Complete IB Economics Activity Book:

52 Complete Units including The Business Cycle, Fiscal and Monetary Policy

Every unit from all four modules: Every topic. Every concept. Every theory. Nothing left out.

900+ Practice Activities

Complete IB Standard Model Answers

IB Standard Marking Schemes

Exam Practice Questions

Always Updated The Living Resource Advantage

The Output Gap: Determining Policy Appropriateness

IB Economics Definition - Output Gap and Policy Appropriateness:

The output gap measures the difference between actual and potential output. A negative output gap (recessionary gap) indicates spare capacity, cyclical unemployment, and low inflationary pressure - conditions under which demand expansion is appropriate and likely to raise real output. A positive output gap (inflationary gap) indicates output above sustainable potential - conditions under which the same demand expansion would generate inflation rather than output gains.

The output gap is a crucial factor to consider when assessing macroeconomic policy in IB Economics. The same fiscal or monetary expansion that proves effective during a recession can lead to negative and inflationary effects during a period of economic growth. Not identifying the position of the output gap before analysing a policy is a frequent mistake that can significantly impact your grade in Paper 1.

A suitable analytical sequence to approach these questions should be like this:

Step 1: Identify the output gap position. Is actual output below, at, or above potential? Is unemployment above, at, or below the natural rate?

Step 2: Identify the type of problem. Is the unemployment/inflation/deficit cyclical (arising from the gap) or structural (independent of the gap)?

Step 3: Match the policy to the problem. Demand-side policy (fiscal or monetary expansion) closes a recessionary gap. Supply-side policy addresses structural problems. Contractionary policy closes an inflationary gap. If you mix these up in your answer - applying demand stimulus to a structural problem, or imposing austerity during a recession - you will probably drop marks for applying the wrong policy and misinterpreting the economic context.

The recession of 2008-09 serves as a clear example of this process. During this period, many developed economies faced a significant recessionary gap, with actual output falling well below potential levels. The result was a surge in cyclical unemployment and a decline in inflationary pressures. Consequently, the substantial fiscal expansions and monetary easing implemented in 2008-09 were justified, as the remaining available capacity meant that stimulating demand would enhance real output rather than simply driving up prices.

In contrast, applying similar stimulus measures in 2021, when supply chain disruptions had diminished potential output and fiscal support had already bolstered demand during the pandemic, led to inflationary pressures. This was because the output gap had either closed or shifted to a positive state in many economies, leaving no productive room for additional demand.

IB Economics Monetary Policy - Full Guide →

IB Economics Supply-Side Policy - Full Guide →

IB Economics fiscal Policy - Full Guide →

Procyclical vs Countercyclical Policy: The Political Economy Problem

IB Economics Definition - Procyclical and Countercyclical Policy:

Countercyclical policy deliberately offsets the business cycle - expanding aggregate demand during recessions and contracting it during booms. Procyclical policy amplifies the cycle - expanding during booms and contracting during recessions. Automatic stabilisers are inherently countercyclical; discretionary policy aims to be countercyclical but often becomes procyclical in practice due to time lags, political incentives, and fiscal rules.

An important evaluation point in the IB Economics syllabus is the connection between the business cycle theory and the real-world limitations of fiscal policy, particularly the difference between countercyclical and procyclical policy outcomes.

Fiscal policy should ideally operate in a countercyclical manner. During economic booms, governments ought to run surpluses to help reduce demand when the economy is performing at or above its potential. Conversely, during recessions, they should run deficits to support demand when there is a negative output gap. Automatic stabilisers, such as progressive taxation and unemployment benefits, serve this purpose and act as efficient countercyclical tools.

Often discretionary fiscal policy does not operate as countercyclical in practice. Political incentives tend to lack balance: governments can easily promote expansion during recessions, as stimulus measures are often well-received by prospective voters. However, justifying contraction during economic booms may be challenging, as raising taxes or reducing spending when the economy seems robust can be politically unpopular. This leads to a consistent trend of procyclical discretionary fiscal policy, or at the very least, insufficient countercyclical measures during expansions, resulting in limited fiscal capacity for future recessions.

Students should explore this political problem when approaching IB Economics exams and assessments as it is a perfectly valid evaluation point. It explains why many economists prefer rules-based fiscal systems - structural balance rules, independent fiscal councils - over discretionary policy: the rules constrain the political incentives that constantly encourage procyclical behaviour.

Reading Economic Indicators: The Paper 2 Skill

IB Economics - Economic Indicators and the Business Cycle:

Leading indicators, such as business confidence surveys, increased orders, the start of new residential buildings, and equity (share) prices, change before GDP and provide insights into the characteristics of oncoming economic cycles. Other indicators, including employment levels, retail sales, and industrial output, move at the same time as the current GDP. Lagging indicators, such as unemployment rates, CPI inflation, and long-term interest rates, confirm a cycle phase after it has taken place. In IB Economics Paper 2, students often have to deal with questions asking them to identify the current phase of the economic cycle and assess the most suitable policy responses.

Therefore, mastering what each indicator provided in the exam context means - such as GDP growth rates, unemployment trends, inflation figures, and levels of business and consumer confidence - is essential. Students should produce a clear assessment of the different indicators, be able to understand the current cycle position, and provide a summary of the most effective policies that could be applied to this context. This system is a basic skill needed to deal with these type of questions in IB Economics.

The key to reading exam indicators correctly is to understand their timing relative to the business cycle. When a data response shows GDP growth turning negative alongside falling business confidence and rising new unemployment, but inflation still elevated from the previous expansion - this is the early recession phase: Why? Because the leading indicators have turned negative, but the lagging inflation indicator has not yet responded. In this case the appropriate policy would be a demand-side stimulus (the output gap is opening), but applying monetary policy would not work in an economic context that still has medium to high inflation (the central bank faces a genuine trade-off).

On the other hand, when GDP growth is accelerating, employment is near its pre-recession level, and inflation is beginning to rise above target - this signals the late recovery or early inflationary gap phase: the most suitable response would be to begin withdrawing stimulus, even though the expansion is ongoing, to prevent the positive output gap from generating long-term inflation.

Some of my students often make the following analytical error and recommend a continued expansion because "the recovery is not complete" - ignoring that the economy is at or approaching potential output, so this would not be right as if we apply further demand expansion this would produce higher inflation rather than output gains.

IB Economics - Syllabus and Programme Full Guide →

External Shocks and Cycle Disruption

Another concept worth mentioning for IB Economics examinations is the distinction between demand-side and supply-side shocks and their value as disruptions to the business cycle.

A demand-side shock - a collapse in consumer confidence, a financial crisis that reduces credit availability, a sharp fall in export markets - shifts the AD curve to the left, creating a recessionary gap with falling output, rising unemployment, and downward pressure on inflation. The standard countercyclical response - fiscal or monetary expansion to shift AD back to the right - is clearly appropriate: it addresses the cause of the gap directly. Source visit: IB Economics Diagrams

A supply-side shock - a sharp rise in energy prices, a pandemic that disrupts production, a technology disruption that reduces productive capacity in key sectors - shifts the SRAS or LRAS curve to the left, creating a different combination: output falls and inflation rises simultaneously (stagflation). Demand-side stimulus in this environment is less appropriate: expanding AD when supply has contracted will worsen inflation rather than restore output. The policy trade-off is clear - accepting higher unemployment to control inflation, or tolerating higher inflation to limit unemployment - and cannot be solved by applying the standard countercyclical playbook without first identifying the nature of the shock. Source visit: IB Economics Diagrams

The 1970s oil price shocks are still good IB Economics examples: developed economies applied demand stimulus to what was fundamentally a supply-side shock, producing stagflation rather than recovery. The correct analytical response was supply-side adjustment - improving energy efficiency, diversifying energy sources, accepting some structural unemployment as the economy adjusted to permanently higher energy costs - rather than demand expansion that the supply constraint prevented from generating greater output gains.

The Analytical Checklist for Business Cycle IB Economics Questions

When an IB Economics Paper 1 or IB Economics Paper 2 question involves the business cycle and macroeconomic policy, try to follow this approach before writing:

1. Identify the output gap position from the data provided - negative (recessionary), zero (at potential), or positive (inflationary). This determines which direction policy should move.

2. Distinguish cyclical from structural - is the unemployment/deficit/slowdown a temporary cycle or a permanent structural feature? Demand policy addresses cyclical problems; supply-side policy addresses structural ones.

3. Identify the shock type if relevant - demand-side or supply-side? Supply-side shocks create stagflation trade-offs that expanding demand cannot resolve cleanly.

4. Evaluate policy effectiveness in context - the same policy produces different outcomes at different cycle phases. Fiscal multipliers are larger during recessions with spare capacity; monetary expansion is constrained when inflation is already high.

5. Acknowledge political economy constraints - discretionary policy frequently becomes procyclical in practice; automatic stabilisers are more reliable countercyclical instruments; fiscal rules attempt to constrain procyclical political incentives.

IB Economics Diagrams Programme, What's included:

200+ exam-ready diagrams covering the entire IB Economics syllabus

Video for every diagram showing you exactly how each model looks

Image version perfect for modelling diagrams in you essays, presentations, and your IA

Detailed written explanations of the IB Economics theory behind each diagram

Both SL and HL IB Economics diagrams clearly labelled and organised by topic

Real IB Economics exam application showing how to use diagrams effectively in Paper 1 and Paper 2

Frequently Asked Questions - Business Cycle and Policy Analysis (IB Economics)

What is the difference between cyclical and structural unemployment in IB Economics?

Cyclical unemployment arises from deficient aggregate demand during a recession - it falls automatically as the economy recovers. Structural unemployment reflects a persistent skills mismatch or sectoral shift, present regardless of the cycle phase. Demand-side policy can address cyclical unemployment by closing the output gap; it cannot address structural unemployment, which requires supply-side interventions such as retraining and education reform. Identifying which type is present before recommending policy is essential for high-band IB responses.

What is a cyclical budget deficit and how does it differ from a structural deficit?

A cyclical deficit is caused by the automatic fall in tax revenues and rise in transfers during a recession - it closes automatically during recovery. A structural deficit persists even at potential output, reflecting a fundamental spending-revenue imbalance. The distinction matters for policy: a cyclical deficit does not necessarily require immediate fiscal adjustment; a structural deficit requires deliberate consolidation even during recovery because it will not self-correct.

How does the output gap determine the appropriate macroeconomic policy response?

A negative output gap justifies demand expansion - spare capacity means stimulus raises real output rather than prices. A positive output gap warrants contractionary policy - output above potential generates inflationary pressure that demand expansion would worsen. The output gap assessment should precede any policy recommendation in IB Economics essays; failing to specify the gap position before evaluating policy is among the most penalised analytical errors in Paper 1 responses.

What is the difference between procyclical and countercyclical policy in IB Economics?

Countercyclical policy offsets the cycle - expanding during recessions, contracting during booms. Procyclical policy amplifies it. Automatic stabilisers are reliably countercyclical; discretionary fiscal policy often becomes procyclical in practice because political incentives favour expansion during both booms and recessions. Rules-based fiscal frameworks attempt to constrain this political economy problem.

How do you read economic indicators to identify the business cycle phase?

Leading indicators (business confidence, new orders, housing starts) signal future GDP movements. Coincident indicators (employment, retail sales) move with current GDP. Lagging indicators (unemployment rates, CPI) confirm phases after they have occurred. In IB Paper 2 data response questions, combining these indicators - noting which have turned and which have not - allows identification of the current phase and appropriate policy inference.

More information about:

IB Economics your IB Economics daily guide

IB Economics Macroeconomics for Business Cycle, Fiscal and Monetary policy contents

IB Economics Diagrams Check Unit 15 for the Business Cycle, Unit 22 for Monetary Policy and Unit 23 for All Fiscal Policy related diagrams and explanations

IB Economics Inflation need to have solid inflation theory base when discussing contractionary fiscal policy and inflationary gaps

IB Economics Activity book Module 3 Macroeconomics Unit 3.4 for the Business Cycle, Unit 3.14 for Fiscal Policy, and Unit 3.15 for Monetary Policy exam practice, activities, model answers and IB Economics Marking schemes

IB Economics The Business Cycle is directly related to countercyclical policy and automatic stabilisers

IB Economics Aggregate Demand and IB Economics Aggregate Supply - Content you need to master in order to understand the effect of the business cycle, revise this theory

IB Economics Fiscal Policy for exploring in depth fiscal responses to the Business Cycle.

IB Economics Monetary Policy learn how monetary policy can help through the different business cycle stages

IB Economics Unemployment contains IB Economics important concepts when discussing expansionary policy and cyclical unemployment

IB economics Calculations Book make sure you check unit 15 for the Business Cycle, unit 21 for Monetary Policy and unit 22 for Fiscal Policy calculations exercises, calculation exam-style questions, IB model answers, and IB marking schemes

Read Next: IB Economics Supply

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form