IB Economics Inflation and Its Impact

Discover how inflation affects your purchasing power, creates economic winners and losers, and why it matters for your finances - for IB Economics students.

IB ECONOMICS HLIB ECONOMICS MACROECONOMICSIB ECONOMICSIB ECONOMICS SL

Lawrence Robert

5/16/202510 min read

The Consequences of Inflation in IB Economics: Why Inflation Is Crucial

Target question:

What are the consequences of inflation in IB Economics?

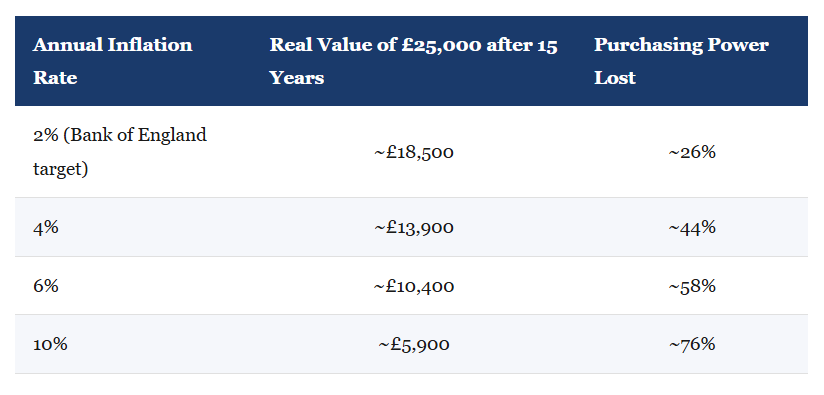

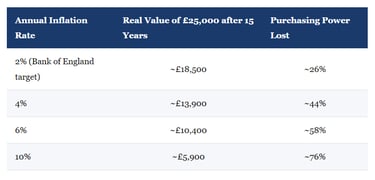

Let's imagine a pensioner who retired on a fixed income of £25,000 a year. Comfortable enough right? - until inflation quietly starts doing its work. At a 2% annual inflation rate, that pension will have lost roughly a quarter of its purchasing power within fifteen years. At 6% - the kind of inflation the UK experienced in 2022 - the pension loses more than half of its value. The money is still there. The number on the giro hasn't changed. But the purchasing power of that same amount has been wiped out. This is why inflation sits at the heart of IB Economics Unit 3 Macroeconomics, and why central banks treat it as one of the most significant indicators in the entire economy.

Every episode of Pint-Sized links back to what matters most for your IB Economics course:

Understanding key IB Economics concepts

Applying them in real-world IB Economics contexts

Building IB Economics course confidence without drowning in dry theory.

Subscribe for free to exclusive episodes designed to boost your IB Economics grades and confidence

1. What Is Inflation? The IB Economics Definition

IB Economics definition - Inflation:

A sustained increase in the general price level of goods and services in an economy over a period of time, resulting in a fall in the purchasing power of money.

IB Economics definition - Consumer Price Index (CPI):

The primary inflation measuring method used in IB Economics. The CPI tracks changes in the price of a representative basket of goods and services purchased by a typical household, expressed as a percentage change over time.

IB Economics definition - Purchasing Power:

The quantity of goods and services that a unit of money can buy. When inflation rises, purchasing power falls - each pound, dollar, or euro buys less than it did before.

The IB Economics syllabus also requires you to understand the two main causes of inflation before evaluating its consequences - because depending on the cause of inflation it will affect the economy differently and will also determine which policies are appropriate in response.

IB Economics definition - Demand-Pull Inflation:

Inflation caused by excess aggregate demand in the economy. When total spending rises faster than the economy's productive capacity, prices are pulled upward. Associated with periods of strong economic growth or expansionary policy.

IB Economics definition - Cost-Push Inflation:

Inflation caused by rising production costs - typically wages, energy, or raw materials - which shift aggregate supply to the left, pushing prices up while output falls. The 2022 UK inflation episode, driven largely by energy and commodity price shocks following the war in Ukraine, was predominantly cost-push in nature.

Lawrence's notes:

In IB Economics Paper 1 and IB Economics Paper 2, clearly distinguishing demand-pull from cost-push inflation before discussing consequences and possible remedying policies is a mark-earning habit. The consequences of inflation can differ depending on the cause - and the appropriate policy response certainly changes too. An examiner expects you to show this awareness rather than treating all inflation as identical.

IB Economics Related entry: For full coverage of the causes of inflation including AD/AS diagram analysis, see IB Economics Inflation & CPI Explained

2. Consequence 1: Purchasing Power Deterioration

The most immediate consequence of inflation is that money loses its value over time. A given nominal income - the amount shown on your payslip - buys progressively fewer real goods and services as prices rise. The table below illustrates how inflation compounds over fifteen years, using the pensioner example from our opening:

Two percentage points of additional inflation - the difference between 2% and 4% - costs this pensioner the equivalent of roughly £4,600 in annual purchasing power after fifteen years. This is not just a simple calculation. It represents real choices: heating or food, medication or rent. The groups most exposed to purchasing power deterioration are those on fixed or slow-adjusting incomes - pensioners, minimum wage workers, and anyone whose wages fail to keep pace with rising prices.

IB Economics Real-life Example:

The UK's inflation rate peaked at over 11% in late 2022 - the highest in forty years - driven primarily by energy and food price shocks. For households on fixed incomes or in receipt of benefits that had not yet been uprated, this represented a significant real-terms fall in living standards. The Bank of England responded by raising interest rates from 0.1% to over 5% between 2022 and 2023 - one of the fastest tightening cycles in its history.

3. Consequence 2: Redistribution - Inflation Creates Winners and Losers

Inflation does not affect everyone equally - it systematically redistributes real income and wealth between different groups. This is one of the most important and most examined consequences in IB Economics.

Winners from Inflation

Borrowers on fixed-rate loans. If you borrowed at a fixed interest rate of 5% when inflation was 2%, a rise in inflation to 6% means the real interest rate becomes negative. The money you repay is worth less than the money you borrowed.

Asset owners. Holders of property, equities, and physical assets often see the nominal value of their assets rise with or above inflation - protecting real wealth.

Governments with large national debts. Inflation erodes the real value of government debt, making it cheaper to service in real terms.

Firms with pricing power. Companies able to raise prices ahead of their own cost increases can protect or improve profit margins during inflationary periods. For instance, petrol stations and governments (through petrol taxes) can make a lot of money in a few days, considering the fact they have bought their product at a cheap price usually months in advance, have the ability to store it and are able to sell it to you at a high price once prices go up triggered by inflation. Those first few inflationary weeks those petrol companies and their governments, can make huge amounts of money.

Losers from Inflation

Savers holding cash. The real value of cash savings falls when inflation exceeds the interest rate paid on deposits - a phenomenon economists call "negative real interest rates."

Fixed income recipients. Pensioners, benefit recipients, and minimum wage workers whose nominal incomes do not automatically adjust upward see their real incomes fall.

Lenders and creditors. Anyone owed a fixed nominal sum - a bank, a bondholder, a friend who lent you money - receives repayment in money worth less in real terms than the amount that was originally lent.

Workers in weak bargaining positions. Where trade unions are weak or wage negotiations are unstable, workers may experience sustained real wage cuts during high inflation periods.

It is worth noting that inflation does not affect all goods and services equally either. The price of housing may fall while energy and food prices rise sharply - meaning that even within the "winners" and "losers" categories, individual cases vary enormously depending on consumption patterns and asset holdings.

IB Economics Exam notes:

The winners and losers section connects directly to the IB Economics key concept of equity. Inflation tends to be regressive - lower-income households spend a higher proportion of their income on essentials (food, energy, transport), which are often the type of goods rising prices the fastest during inflationary episodes. This makes high inflation not just an efficiency concern but an equity concern, which strengthens the case for active inflation management by central banks.

IB Economics - Syllabus and Programme Full Guide →

4. Consequence 3: Uncertainty and Shortened Planning Horizons

When inflation is high or unpredictable, it becomes difficult for firms, households, and governments to plan ahead. An airline negotiating a multi-year wage contract with its pilots needs to form a view about what those wages will be worth in real terms three or five years from now. A construction firm tendering for a long-term infrastructure contract must estimate the future costs of materials. A household considering a thirty-year mortgage must judge whether their income will keep pace with prices over the entire period.

High and volatile inflation makes all of these calculations unreliable. The result is that economic agents shorten their planning horizons - firms invest less in long-term capital projects, banks become reluctant to issue long-term loans at fixed rates, and households prioritise holding real assets (property, gold, foreign currency) over financial investments. This reduction in long-term investment crushes economic growth.

In countries that have experienced hyperinflation - the Weimar Republic in the 1920s, Zimbabwe in the 2000s, Argentina across multiple episodes - this uncertainty becomes so severe that the domestic currency loses entirely its function as a store of value and medium of exchange, causing deep economic disruption that takes years to reverse.

Lawrence's notes:

A common error among some of my students is to assume that predictable inflation is harmless. In fact, even perfectly anticipated inflation carries real costs - it forces firms and households to devote resources to managing inflation rather than productive activity (economists call these "menu costs" and "shoe-leather costs" IB Economics HL). The IB syllabus expects IB Economics SL students to identify uncertainty as a key negative consequence; HL students should be able to explain the additional welfare costs of anticipated inflation.

5. Consequence 4: Loss of International Competitiveness

If a country's inflation rate is persistently higher than that of its trading partners, its exports become relatively more expensive on world markets while imports become relatively cheaper. This damages the international competitiveness of domestic producers, reduces export revenue, and increases import expenditure - worsening the current account of the balance of payments.

This is particularly significant for countries in a fixed exchange rate system or monetary union - such as Eurozone members - where the exchange rate cannot automatically depreciate to restore competitiveness. A country like Greece, which experienced relatively high inflation in the years before the 2010 debt crisis, found its export sector increasingly uncompetitive against Germany without the option of devaluing its currency.

Related entry: For full coverage of exchange rates and international competitiveness, see:

IB Economics Exchange Rates - Full Guide →

6. Deflation: The Other Side of the Coin

It is tempting to assume that falling prices - deflation - must be the opposite of the problem. In fact, deflation carries its own serious economic risks, and the IB Economics syllabus requires you to understand why.

IB Economics definition - Deflation:

A sustained decrease in the general price level, resulting in a rise in the real value of money over time.

When prices are falling, consumers and firms have an incentive to delay purchases and investment - why buy or take a risk today when it will be cheaper tomorrow? This deferral of spending reduces aggregate demand, which causes output and employment to fall further, which in turn causes prices to fall further still. This self-reinforcing cycle is known as a deflationary spiral and can be extremely difficult for policymakers to reverse, as Japan's experience across the 1990s and 2000s demonstrated. Most central banks therefore target a low but positive inflation rate - the Bank of England targets 2% CPI - precisely to maintain a buffer against deflationary risk.

IB Economics Deflation - Full Guide →

IB Economics Diagrams Programme, What's included:

200+ exam-ready diagrams covering the entire IB Economics syllabus

Video for every diagram showing you exactly how each model looks

Image version perfect for modelling diagrams in you essays, presentations, and your IA

Detailed written explanations of the IB Economics theory behind each diagram

Both SL and HL IB Economics diagrams clearly labelled and organised by topic

Real IB Economics exam application showing how to use diagrams effectively in Paper 1 and Paper 2

Frequently Asked Questions: Inflation in IB Economics

Q: What are the consequences of inflation in IB Economics?

In IB Economics, the main consequences of inflation are: (1) erosion of purchasing power - inflation reduces the real value of money, disproportionately harming those on fixed or slow-adjusting incomes; (2) redistribution of income and wealth - inflation creates winners (borrowers, asset owners, governments with large debts) and losers (savers, fixed income recipients, lenders); (3) uncertainty and shortened planning horizons - high or unpredictable inflation makes long-term investment decisions unreliable, reducing economic growth; and (4) loss of international competitiveness - if domestic inflation exceeds that of trading partners, exports become relatively more expensive, worsening the current account balance.

Q: What is the difference between demand-pull and cost-push inflation in IB Economics?

Demand-pull inflation occurs when aggregate demand in the economy rises faster than productive capacity, pulling prices upward - typically associated with strong economic growth or expansionary government policy. Cost-push inflation occurs when rising production costs (energy, wages, raw materials) shift aggregate supply to the left, pushing prices up while output falls simultaneously. The distinction matters in IB Economics because the causes of inflation determine which policy responses are appropriate - and because cost-push inflation creates the particularly difficult combination of rising prices and falling output known as stagflation.

Q: Why does inflation create winners and losers in IB Economics?

Inflation redistributes real income and wealth because it affects different economic agents differently. Borrowers on fixed-rate loans benefit because they repay in money that is worth less in real terms than what they borrowed. Asset owners benefit as the nominal value of property and equities tends to rise with inflation. Conversely, savers holding cash lose purchasing power when inflation exceeds interest rates, and fixed income recipients - pensioners, minimum wage workers - see their real incomes fall if nominal incomes do not adjust upward. This redistributive effect is why high inflation is considered an equity concern in IB Economics, not just an efficiency concern.

Q: How is inflation measured in IB Economics?

In IB Economics, inflation is primarily measured using the Consumer Price Index (CPI). The CPI tracks changes in the price of a representative basket of goods and services typically purchased by households, expressed as a percentage change over time. A rise in the CPI indicates that the average price level has increased - and therefore that the purchasing power of money has fallen. Most central banks, including the Bank of England, use CPI as the basis for their inflation targets (the UK target is 2% annual CPI inflation).

Q: Why is deflation a problem in IB Economics?

Deflation - a sustained fall in the general price level - is problematic in IB Economics because it can trigger a deflationary spiral. When prices are expected to fall further, consumers and firms delay spending and investment, reducing aggregate demand. This fall in demand causes output and employment to decline, which puts further downward pressure on prices, reinforcing the cycle. Deflation also increases the real burden of debt - borrowers must repay in money worth more than what they borrowed. Japan's experience of prolonged deflation in the 1990s and 2000s illustrates why most central banks target a low but positive inflation rate rather than zero inflation.

Explore Topics:

IB Economics your IB Economics daily guide

IB Economics Macroeconomics low inflation is one of the main macro objectives together with, low unemployment, sustainable economic growth, and equitable distribution of income

IB Economics Diagrams Check Unit 19 for All inflation diagrams with explanations

IB Economics Activity book Module 3 Macroeconomics Unit 3.12 for low inflation exam practice, activities, model answers and IB Economics Marking schemes

IB Economics Unemployment is directly related to cost-push inflation (falling output + rising prices = rising unemployment risk), revise this theory

IB Economics Monetary Policy for exploring in depth Monetary Policy / Interest Rates and the real interest rate / savers comment.

IB economics Calculations Book make sure you check unit 19 for low inflation calculations exercises, IB model answers, and IB marking schemes

IB Economics Inflation here you will find all the information and content you need on inflation

Read Next: IB Economics The Evolution of Money

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form