IB Economics Monetarist vs Keynesian Covered

Keynes vs Monetarists: who rules the macroeconomy? A fun dive into economic policy, sticky wages, and real-world shocks explained for IB Economics students

IB ECONOMICS HLIB ECONOMICS MACROECONOMICSIB ECONOMICSIB ECONOMICS SL

Lawrence Robert

4/24/202512 min read

Keynesian vs Monetarist: Why Assumptions Change Everything in IB Economics

Target Question:

What is the difference between Keynesian and Monetarist assumptions in IB Economics?

Imagine two economists walk into a pub. One orders a pint and says: "When things go wrong, the government needs to step in." The other sips a black coffee and replies: "Let the market fix itself." They are not having a disagreement about facts. They are having a disagreement about assumptions - specifically, about whether wages fall quickly or slowly when unemployment rises. And from that single difference, everything else follows.

This is the Keynesian vs Monetarist debate, and it is one of the most popular topics in IB Economics assessment because it demonstrates something that runs through the entire course: your conclusions depend entirely on your starting assumptions. Change the assumption, and the policy prescription reverses.

This entry covers the assumptions debate itself - why Keynesians and Monetarists reach such different conclusions from the same starting observation (an economy in recession).

For the causal theories of why recessions happen, see our recessions guide entry. For the Keynesian policy toolkit in detail, see our countercyclical fiscal policy entry IB Economics Fiscal Policy Expansionary & Contractionary

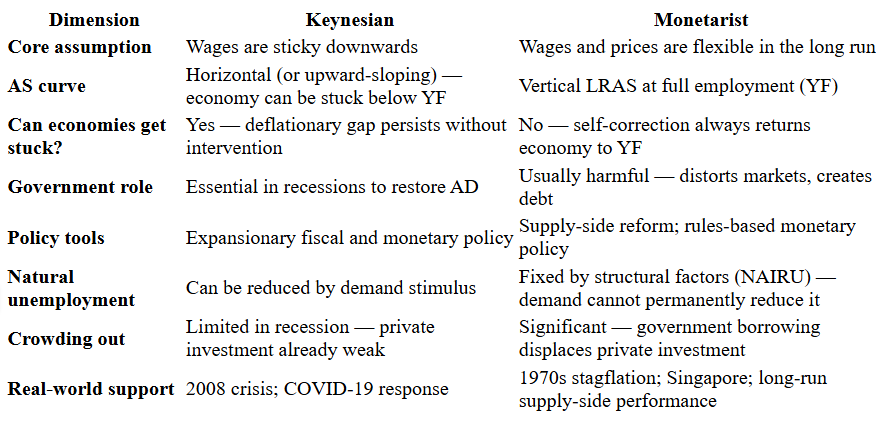

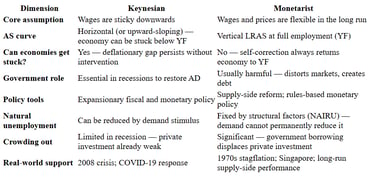

The Main Assumption: Do Wages Fall When Unemployment Rises?

Both Keynesians and Monetarists agree on the basic functioning of a recession: aggregate demand falls, output falls, unemployment rises. Where they disagree - entirely and consequentially - is on what happens next in the labour market.

IB Economics Definition - Sticky Wages:

Sticky wages (or downward wage rigidity) is the Keynesian assumption that nominal wages resist falling even when unemployment rises and labour markets have excess supply. Workers and unions resist pay cuts, and contracts, social norms, and the productivity effects of wage cuts reinforce this resistance. Sticky wages mean the labour market does not clear quickly in a recession, producing persistent unemployment rather than rapid self-correction.

Have you ever tried telling a footballer they will earn less this season for the same performance? Or asking a teacher to accept a 10% pay cut because it would "restore macroeconomic equilibrium"? That is the problem Keynes identified. Workers resist wage reductions - not because they are irrational, but because pay cuts are demoralising, contracts make cuts legally difficult, and one of the main reasons trade unions exist is to prevent these cuts. This resistance is particularly strong when wages go down: wages rise readily in booms but are sticky in recessions.

The consequences for macroeconomic analysis are significant. If wages are sticky, a fall in aggregate demand produces unemployment - not wage adjustment. Employers face reduced demand for their output, but cannot cut wages to match the new context; instead, they cut employment. The labour market does not clear. Unemployment persists. And because unemployed workers have less income, their spending falls further, deepening the recession through the multiplier working in reverse.

Keynes's insight was that this could be a stable trap or tendency, not a temporary flaw. An economy with sticky wages can sit in a deflationary gap - output below potential, unemployment above the full employment level - indefinitely, because the automatic self-correction mechanism (falling wages restoring employment) is blocked.

Complete IB Economics Activity Book:

52 Complete Units including the Keynesian vs. Monetarist Arguments

Every unit from all four modules: Every topic. Every concept. Every theory. Nothing left out.

900+ Practice Activities

Complete IB Standard Model Answers

IB Standard Marking Schemes

Exam Practice Questions

Always Updated The Living Resource Advantage

The Keynesian Equilibrium Below Full Employment

IB Economics Definition - Keynesian Equilibrium Below Full Employment:

The Keynesian equilibrium below full employment occurs when sticky wages prevent the labour market from clearing, leaving the economy in a persistent deflationary (recessionary) gap. Because wages will not fall to eliminate unemployment, the economy does not self-correct to full employment without external stimulus. This provides the Keynesian justification for government intervention to restore aggregate demand.

In the AD/AS framework, sticky wages produce a short-run aggregate supply curve with a horizontal (or near-horizontal) section at low levels of output. When the economy is below full employment and has significant spare capacity, an increase in aggregate demand raises output without raising prices - because unemployed workers can be hired at the existing wage without bidding wages up, and idle capital can be brought back into production without additional cost pressure. The economy is on the flat section of the Keynesian AS curve. Source visit: IB Economics Diagrams

This has a highly significant implication: fiscal stimulus in a Keynesian world raises real output. A government that increases spending or cuts taxes shifts the AD curve to the right, and - on the flat section of the AS curve - the economy moves toward full employment at stable prices. The multiplier amplifies the initial stimulus. Employment rises. Income rises. The economy climbs out of the deflationary gap.

Without that intervention, the sticky wages assumption means the economy stays stuck. The Great Depression of the 1930s - which lasted for a decade and that only moved forward with the massive demand injection of wartime spending - is the historical case that gave Keynes's framework its empirical authority. As he observed: "In the long run, we are all dead." Waiting for wages to eventually fall enough to restore full employment is not an acceptable policy if the adjustment takes a decade.

The Monetarist Challenge: Markets Self-Correct

IB Economics Definition - Monetarist LRAS:

The Monetarist long-run aggregate supply (LRAS) curve is vertical at the full employment level of output (YF). It reflects the assumption that wages and prices are flexible in the long run, allowing markets to self-correct to full employment regardless of the level of aggregate demand. Any position below YF is temporary - falling wages will restore full employment without government intervention.

Milton Friedman and the Monetarists looked at the same labour market and reached a different conclusion. Yes, wages are sticky in the very short run. But in the long run - as contracts expire, as social norms adjust, as the reality of persistent unemployment forces workers to accept lower wages - wages will fall. When they do, employers start hiring again. The economy self-corrects back to full employment.

In the AD/AS diagram, this produces a vertical long-run aggregate supply curve at the economy's full employment output level (YF). This is the Monetarist LRAS: a supply curve that does not respond to changes in aggregate demand at all, because in the long run, the economy always gravitates back to YF regardless of where AD sits. A fall in AD creates a temporary recessionary gap, but the self-correction mechanism - falling wages, rising employment - closes it without any need for government action. Source visit: IB Economics Diagrams

The implication of this is clear: Keynesian fiscal stimulus is at best unnecessary and at worst harmful. If the economy is going to self-correct anyway, government spending only adds public debt and creates a distorted reality regarding relative prices without producing any lasting output gain. And if the government borrows to finance the stimulus, it may crowd out private investment in the process.

IB Economics - Syllabus and Programme Full Guide →

Crowding Out: The Monetarist Case Against Fiscal Expansion

IB Economics Definition - Crowding Out:

Crowding out is the Monetarist argument that government borrowing to finance fiscal expansion raises interest rates in the loanable funds market, reducing private sector investment. If the rise in interest rates offsets the fiscal stimulus, the net effect on aggregate demand is reduced or eliminated - making expansionary fiscal policy less effective than Keynesians predict and potentially harmful to long-run growth by displacing more productive private investment with less efficient government spending.

The crowding out argument is as follows. When the government borrows to finance a fiscal stimulus, it enters the market for loanable funds as a large borrower. This increased demand for funds pushes up interest rates. Higher interest rates raise the cost of borrowing for private firms - reducing their investment plans. If every pound the government injects through fiscal expansion displaces a pound of private investment, the net effect on aggregate demand is zero. The economy is not better off, but public debt has risen and private capital formation has fallen.

Keynesians counter that crowding out is limited - and possibly absent - in a recession. When the economy is below full employment, private investment demand is already weak. Firms are not investing because they see no profitable opportunities in a depressed economy; they are not being held back by interest rates. Government borrowing in these conditions does not compete significantly for funds that private investors would otherwise use. The crowding out argument is more convincing when the economy is already at or near full employment - those are exactly the conditions when the Keynesian case for stimulus is weakest.

The Natural Rate of Unemployment: The Monetarist Floor

IB Economics Definition - Natural Rate of Unemployment (NAIRU):

The natural rate of unemployment (Non-Accelerating Inflation Rate of Unemployment) is the Monetarist concept of the unemployment rate consistent with stable inflation. It includes frictional and structural unemployment but excludes cyclical unemployment. Monetarists argue that the economy always gravitates toward the natural rate in the long run, and that attempts to push unemployment below it through demand stimulus will only produce accelerating inflation - not permanent employment gains.

Monetarists present an additional argument that limits the effectiveness of government intervention. Although Keynesian stimulus may successfully lower unemployment in the short term, it cannot sustain unemployment below the natural rate without causing escalating inflation. When unemployment dips below the natural rate, the labour market becomes excessively tight. Employers must increase wages to attract workers, which raises costs and prices, ultimately diminishing the real value of any wage increases. As prices rise, workers seek higher wages to offset these increases, further driving inflation upwards.

The Friedman expectations argument suggests that anticipated inflation counteracts demand stimulus. When workers expect inflation, they seek wage increases to offset it, which diminishes any real output gains from the stimulus. To achieve lasting reductions in unemployment, it is essential to tackle its structural and frictional causes through supply-side policies rather than demand management.

The Monetarist Policy Prescription: Supply-Side Reform

When the long-run aggregate supply (AS) curve is vertical and the natural rate of unemployment establishes a minimum threshold that demand policies cannot sustainably lower, governments should consider their approach carefully.

According to Monetarist theory, the recommended strategy is to implement supply-side policies. These measures aim to shift the long-run aggregate supply (LRAS) curve to the right by enhancing the economy's productive capacity and lowering the natural rate of unemployment:

Education and training reduce structural unemployment by improving the match between workers' skills and employers' needs, reducing the natural rate directly. Deregulation and tax reduction improve incentives for private investment and entrepreneurship, expanding potential output. Labour market flexibility - reducing the power of unions to maintain above-equilibrium wages, making hiring and firing easier - speeds up the self-correction process and reduces the frictions that produce frictional unemployment.

IB Economics Regulation and Deregulation - Full Guide →

Singapore consistently exemplifies this approach through its low and predictable tax rates, significant investment in skills and education, an open and competitive economy, and a government that actively avoids deficit spending. As a result, it has achieved sustained productivity growth and low structural unemployment, aligning with the Monetarist view that long-term prosperity relies on supply-side fundamentals rather than demand management.

When the Evidence Sides with Each School

The honest IB Economics answer to "who is right?" is: it depends on the timeframe and the nature of the shock.

The 2008 global financial crisis and the COVID-19 recession strongly support the Keynesian view in the short term. In both instances, aggregate demand fell more quickly than wages or prices could adapt. Without intervention, both recessions would have worsened significantly. The UK's furlough scheme, the US stimulus packages, and fiscal support in the eurozone all helped stabilise demand. The relatively swift recovery, in contrast to the unassisted recovery of the 1930s, indicates that Keynesian demand management was effective during these situations. Wages remained inflexible, and the economy required that boost.

The supply-side stagnation of the 1970s, during which governments attempted to use demand stimulus to maintain unemployment below its natural rate, strongly supports the Monetarist perspective. This approach led to stagflation: an increase in inflation without a decrease in unemployment, exactly as Friedman had initially forecasted. Eventually, governments recognised that they could not sustainably keep unemployment below its structural level. Consequently, the move towards inflation targeting and supply-side reforms in the 1980s and 1990s represented a significant victory for Monetarism.

Current Assessment: Where Both Schools Live Today

Modern macroeconomic policymaking does not choose between Keynes and Friedman - it incorporates both. The New Keynesian framework that dominates central banking accepts the Keynesian insight that wages and prices are sticky in the short run, producing real effects from demand shocks. But it also accepts the Monetarist insight that expectations are incredibly relevant: credible commitments to price stability prevent the inflationary spirals that undermine demand management.

The Bank of England's inflation targeting regime - using interest rates as the primary instrument to stabilise inflation around a 2% target, combined with a willingness to use fiscal policy in severe downturns - summarises this approach. Short-run demand management when the output gap is negative; credible long-run commitment to price stability; structural supply-side reform as the route to permanent productivity improvement.

For IB Economics, the key lesson is primarily a debate about assumptions - specifically about the speed of wage and price adjustment. Understand the assumptions, and the conclusions are inevitable. Change the assumptions, and the conclusions reverse.

What to Write in Your IB Economics Exam

IB Economics Summary

The Keynesian and Monetarist schools do not disagree about the facts of a recession. They disagree about one assumption: whether wages fall quickly enough to restore full employment without government intervention. The Keynesian answer is no - wages are sticky, unemployment persists, intervention is justified. The Monetarist answer is yes - in the long run, markets self-correct, and government intervention only adds distortions and debt.

From that single assumption difference, everything follows: the shape of the AS curve, the effectiveness of fiscal policy, the role of crowding out, the meaning of the natural rate of unemployment, and the appropriate policy toolkit.

In IB Economics, the lesson is not which school is right - historical evidence supports both in different contexts - but that assumptions shape conclusions. Learn the assumptions and you can derive the policy prescriptions yourself. That is the analytical skill your teacher and your examiner are looking for.

IB Economics Diagrams Programme, What's included:

200+ exam-ready diagrams covering the entire IB Economics syllabus

Video for every diagram showing you exactly how each model looks

Image version perfect for modelling diagrams in you essays, presentations, and your IA

Detailed written explanations of the IB Economics theory behind each diagram

Both SL and HL IB Economics diagrams clearly labelled and organised by topic

Real IB Economics exam application showing how to use diagrams effectively in Paper 1 and Paper 2

Frequently Asked Questions - Keynesian vs Monetarist (IB Economics)

What is the difference between Keynesian and Monetarist assumptions in IB Economics?

The central difference is wage flexibility. Keynesians assume wages are sticky downwards - workers resist pay cuts, so the economy can be stuck below full employment in a persistent deflationary gap. Monetarists assume wages and prices are flexible in the long run - markets self-correct to full employment (YF) without intervention. Every policy disagreement between the two schools follows from this foundational difference in assumption.

What are sticky wages in IB Economics?

Sticky wages (downward wage rigidity) is the Keynesian assumption that nominal wages resist falling even when unemployment rises. Workers and unions resist pay cuts, contracts make reductions legally difficult, and wage cuts harm morale and productivity. Sticky wages mean the labour market does not quickly clear in a recession - unemployment persists rather than resolving through wage adjustment - justifying government demand stimulus.

What is the natural rate of unemployment (NAIRU) in IB Economics?

The natural rate of unemployment is the Monetarist concept of the unemployment rate consistent with stable inflation. It includes frictional and structural unemployment but not cyclical unemployment. Monetarists argue governments cannot sustainably reduce unemployment below the natural rate through demand stimulus - attempts to do so produce accelerating inflation rather than lasting employment gains. Only supply-side reforms that reduce frictional and structural unemployment can permanently lower the natural rate.

What is crowding out in IB Economics?

Crowding out is the Monetarist argument that government borrowing raises interest rates, reducing private investment by an amount that partially or fully offsets the fiscal stimulus. Keynesians counter that crowding out is limited in recession because private investment is already weak and interest rates are unlikely to rise significantly when the economy has spare capacity. The debate is therefore context-dependent: crowding out is more significant near full employment, less so in deep recessions.

How does the Keynesian vs Monetarist debate appear in IB Economics exam questions?

Typically in questions about appropriate macroeconomic policy responses to recession or inflation. A strong response identifies the core assumption difference (wage flexibility), derives the AS curve implication (Keynesian horizontal section vs Monetarist vertical LRAS), explains the policy conclusion that follows, evaluates real-world evidence (2008 and COVID supporting Keynesian intervention; 1970s stagflation supporting Monetarist supply-side approach), and acknowledges the New Keynesian synthesis that modern central banks actually use.

Read More About:

IB Economics your IB Economics daily guide

IB Economics Macroeconomics access Monetarist versus Keynesian, Fiscal Policy and Monetary Policy here as well as the rest of module 3

IB Economics Diagrams Check Unit 22 for Monetary Policy and Unit 23 for All Fiscal Policy diagrams with explanations

IB Economics Aggregate Demand essential information when discussing how fiscal policy shifts AD

IB Economics Aggregate Supply Explore this content as the relationship between aggregate supply and macroeconomic theories is related to how each school models an economy's production capacity. Keynesians believe aggregate supply is highly responsive and that output is driven by demand. Monetarists believe supply is fixed in the long run and driven by money supply.

IB Economics Activity book Module 3 Macroeconomics Unit 3.14 for Fiscal Policy and Unit 3.15 for Monetary Policy exam practice, activities, model answers and IB Economics Marking schemes

IB Economics The Business Cycle is directly related to countercyclical policy and automatic stabilisers

IB Economics Monetary Policy for exploring in depth the contrast between Monetary Policy and this entry Fiscal Policy.

IB Economics Unemployment contains IB Economics important concepts when discussing expansionary policy and cyclical unemployment

IB Economics Inflation Hub need to have solid inflation theory base when discussing contractionary fiscal policy and inflationary gaps

IB economics Calculations Book make sure you check unit 21 for Monetary Policy and unit 22 for Fiscal Policy calculations exercises, IB model answers, and IB marking schemes

IB Economics Fiscal Policy for exploring in depth the contrast between Monetary Policy and Fiscal Policy.

Read Next: IB Economics Economic Growth Explained

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form