IB Business Management Toolkit Contribution

Guide to the IB Business Toolkit - Learn Contribution Analysis HL, be able to analyse the profitability of a firm’s goods & services, or specific projects

IB BUSINESS MANAGEMENTIB BUSINESS MANAGEMENT TOOLKITIB BUSINESS MANAGEMENT HL

Lawrence Robert

6/3/20268 min read

Contribution Analysis: The Complete IB Business Management HL Guide

Target Question:

What is contribution analysis in IB Business Management?

In 2019, Nike stopped selling directly on Amazon and invested heavily in its own direct-to-consumer channels. The decision was not only about brand image - it was based on contribution analysis. Nike's margins on Amazon were being compressed by platform fees and discounting; its own website generated significantly higher contribution per unit.

Understanding exactly how much each channel, product, or division contributes to covering overheads is one of the most powerful tools a manager has. This is basically what this topic is about.

This guide covers everything you need for the IB Business Management HL exam: what contribution analysis is, how to apply it to make-or-buy decisions, how contribution costing and absorption costing work, and how to interpret the results. I have also included a full worked example and exam-style practice exercise.

What is Contribution Analysis?

IB Business Management Key Definition:

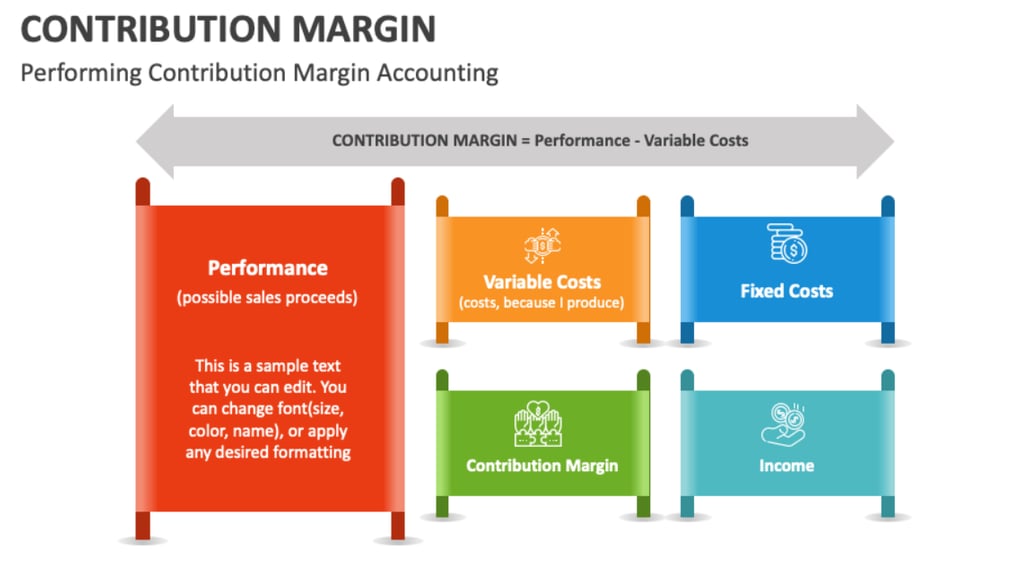

Contribution is the financial surplus remaining after a product's variable (direct) costs are subtracted from its revenue. It represents the amount that each unit of output, or each product line, contributes towards covering the firm's fixed (indirect) costs - and ultimately towards profit.

There are two ways to measure contribution:

Total contribution = Total Revenue (TR) − Total Variable Costs (TVC)

Contribution per unit = Selling Price (P) − Average Variable Cost (AVC)

Once a product generates enough contribution to cover the firm's fixed costs, the business reaches break-even. Any contribution earned beyond that point becomes profit. This makes contribution a precise lens through which managers can evaluate individual products, pricing decisions, and resource allocation.

IB Business Management Break Even Analysis - Full Guide →

Worked Example - Contribution Per Unit

A fitness brand sells resistance bands at $18 each. The variable cost per unit (materials, direct labour, packaging) is $7. Contribution per unit = $18 − $7 = $11. If annual fixed costs are $110,000, the brand needs to sell 110,000 ÷ 11 = 10,000 units to break even. Every unit sold beyond this generates $11 in profit.

Make or Buy Analysis

IB Business Management Key Definition:

Make or buy analysis is a management decision-making tool used to determine whether it is more cost-effective for a business to produce a component or product in-house (the make option) or to purchase it from an external supplier (the buy option). The decision compares the cost to make (CTM) against the cost to buy (CTB).

Quantitative Decision: CTM vs CTB

The starting point is always a straight cost comparison. If CTB < CTM, there is a financial case to outsource. If CTM < CTB, making in-house is cheaper.

Worked Example - Meridian Electronics

Meridian Electronics manufactures 10,000 circuit boards per year. In-house cost: $9 materials + $6 labour + $3 overheads = $18 per unit (CTM = $180,000). An external supplier quotes $15 per unit (CTB = $150,000). Annual saving if outsourced: ($18 − $15) × 10,000 = $30,000. The financial case points to buying.

Qualitative Factors

A make or buy decision is rarely settled by numbers alone. Managers must also weigh:

Quality: Can the supplier match in-house quality standards consistently?

Lead times: An external supplier may require 6 weeks vs. 1 week in-house - problematic for lean production.

Intellectual property: Sharing product specifications with an external supplier creates IP exposure risk.

Supplier reliability: A single supplier creates dependency; supply disruptions halt production.

Core competency: If manufacturing is central to the firm's competitive advantage, outsourcing it undermines the business model.

IB Business Management Exam Technique:

Make or buy questions almost always ask you to consider both quantitative and qualitative factors. Even if the numbers clearly favour one option, a well-evaluated answer will identify at least one qualitative reason as to why the cheaper option might not be the best choice in the specific business context.

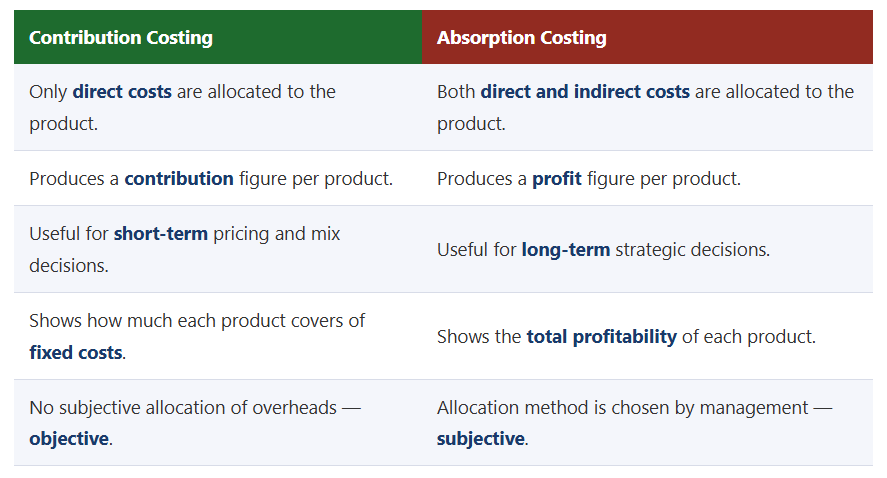

Contribution Costing

IB Business Management Key Definition:

Contribution costing is a method of cost analysis that allocates only direct (variable) costs to individual products or divisions. It calculates how much each product contributes to the firm's fixed costs after covering its own direct costs. The result is the contribution figure - not full profit - for each product.

Contribution costing is used primarily for short-term pricing and product mix decisions. Because indirect costs are not allocated to individual products, it avoids the distortions that are originated from choosing an arbitrary allocation method.

The contribution costing format for a multi-product firm looks like this:

Total contribution ($340,000) must then cover the firm's fixed costs before any profit is made. If fixed costs are $200,000, the firm earns $140,000 profit overall - but contribution costing alone does not tell us which product is most profitable after accounting for overhead.

Absorption Costing

IB Business Management Key Definition:

Absorption costing (also called full costing) extends contribution costing by allocating the firm's indirect (fixed) costs - such as rent, management salaries, and utilities - to each product or division. This produces a profit figure for each product rather than just a contribution figure, giving managers a clearer picture of the firm's full cost structure.

There are two standard methods for allocating indirect costs in the IB Business Management syllabus:

Method 1 - Equal Allocation

Divide total indirect costs equally between all products.

Formula: Indirect cost per product = Total indirect costs ÷ Number of products

Simple and quick to apply

Ignores differences in revenue or resource use

May overstate costs for low-revenue products

Method 2 - Proportional Allocation

Allocate indirect costs in proportion to each product's share of total sales revenue.

Formula: Indirect cost = (Product revenue ÷ Total revenue) × Total indirect costs

More reflective of actual resource demands

Higher-revenue products bear more overhead

More complex to calculate

Lawrence's Notes: The Subjectivity Problem

Neither method is objectively correct. Method 1 treats every product identically regardless of size; Method 2 penalises high-revenue products. A manager using Method 1 might classify a product as unprofitable and discontinue it - but the same product under Method 2 might appear perfectly viable. This subjectivity is a genuine limitation of absorption costing, and can be tested in IB Business Management evaluation questions.

Contribution Costing vs. Absorption Costing

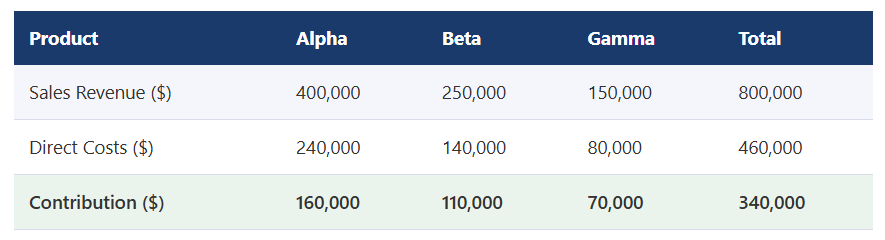

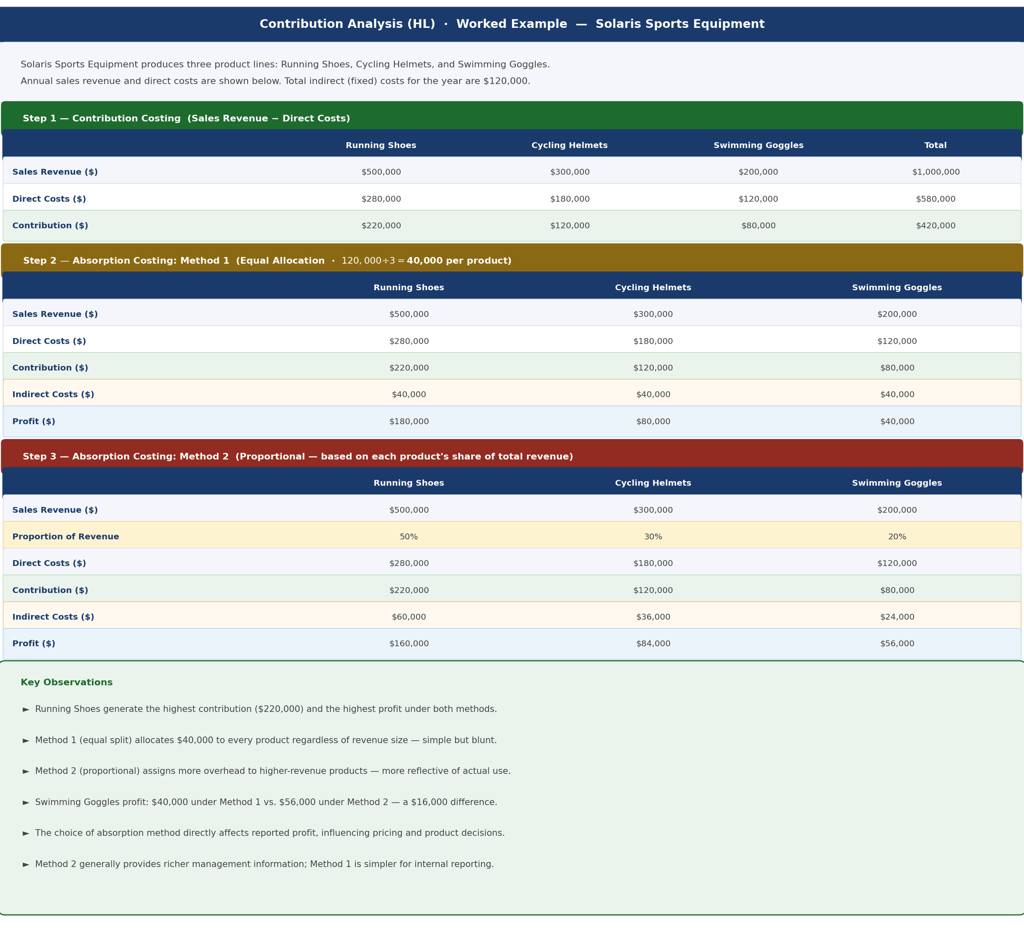

Worked Example - Solaris Sports Equipment

Solaris Sports Equipment produces three product lines. The network below shows the complete step-by-step contribution and absorption analysis, including both allocation methods and a comparison of results.

Figure 1: Contribution and absorption costing for Solaris Sports Equipment. Step 1 shows contribution costing; Steps 2 and 3 show absorption costing using Method 1 (equal allocation) and Method 2 (proportional allocation) respectively.

Reading the Worked Example

Running Shoes generates the highest contribution ($220,000) because it has the largest revenue-to-cost margin.

Under Method 1, all three products bear identical indirect costs ($40,000 each). Swimming Goggles, with the smallest revenue ($200,000), appears least profitable at $40,000.

Under Method 2, Swimming Goggles is only allocated 20% of total indirect costs ($24,000), raising its profit to $56,000 - a more positive picture.

The $16,000 difference in Swimming Goggles' profit between the two methods illustrates how choice of absorption method can influence discontinuation decisions.

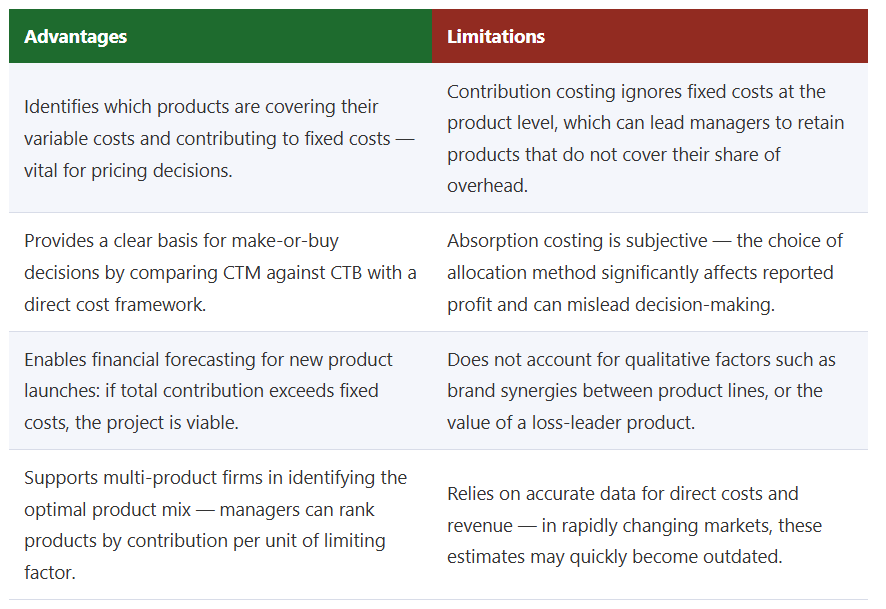

Advantages and Limitations of Contribution Analysis

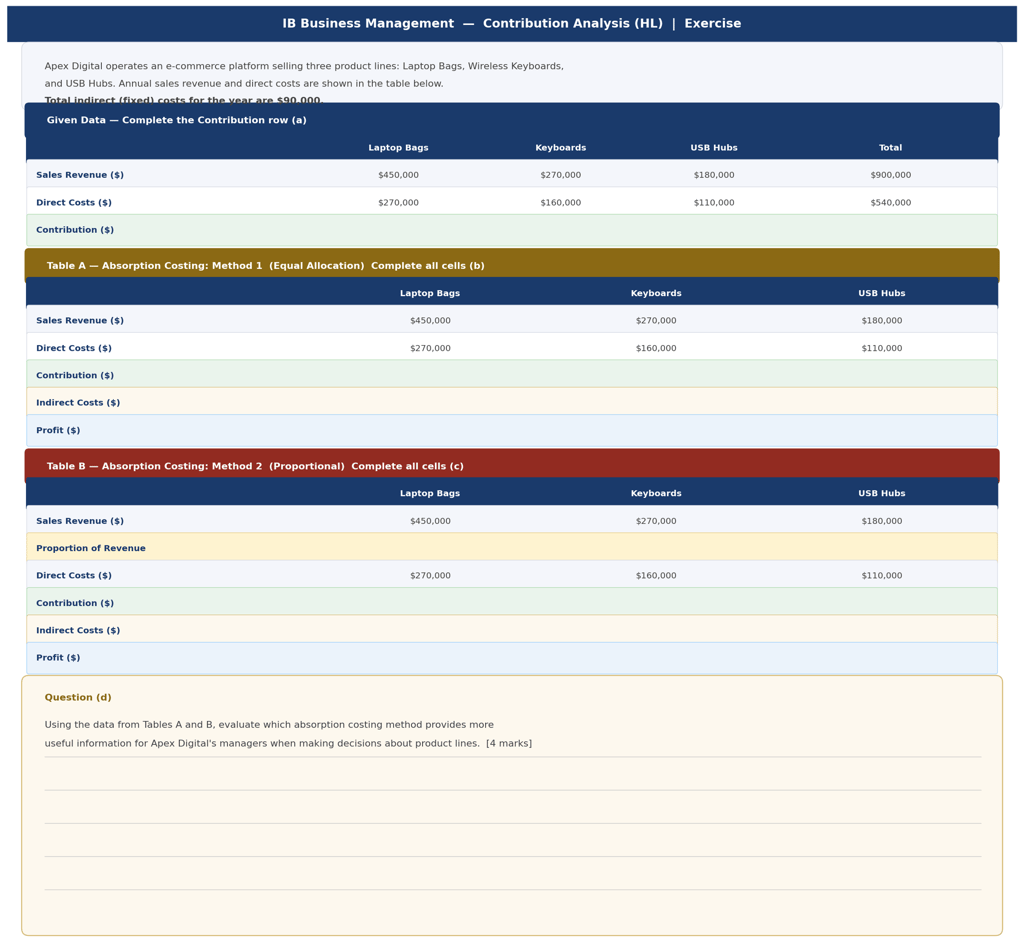

Exam Practice - Apex Digital

Apex Digital operates an e-commerce platform selling three product lines. Complete the contribution and absorption costing tables, then answer the evaluation question.

Figure 2: Exercise for Apex Digital. Complete the Contribution row in the given data table, then fill in Tables A (Method 1) and B (Method 2), and answer the evaluation question.

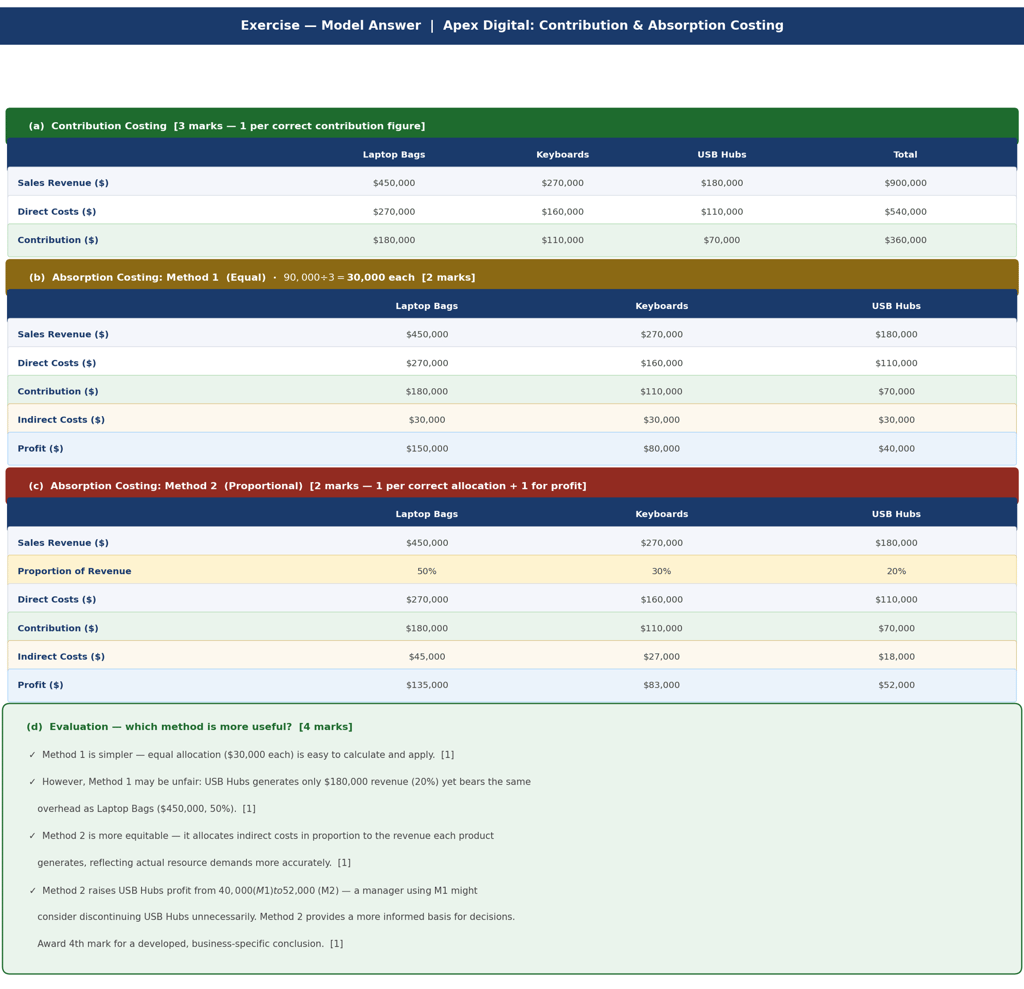

Model Answer

Figure 3: Model answer for Apex Digital. Complete tables for both methods and mark scheme for the evaluation question.

Exam Technique - Contribution Questions

Always show the formula before substituting numbers. Write "Contribution per unit = P − AVC" or "Total contribution = TR − TVC" and then substitute. Method marks are available even if the final answer is wrong.

For absorption costing questions, clearly state which method you are using and show how you calculated each allocation. Examiners need to follow your working, not just your answer.

For evaluation questions (4–6 marks), the strongest responses argue that neither method is definitively superior - Method 1 is simpler but less fair; Method 2 is more equitable but involves a subjective allocation decision. A justified recommendation linked to the firm's context scores the top mark band.

Make or buy evaluation must address both quantitative and qualitative dimensions. Stating only "CTB < CTM, therefore buy" scores at most 2 marks.

Watch the language: contribution is not profit. Contribution covers fixed costs; only what remains after that is profit. Mixing up these terms in the exam loses marks.

Frequently Asked Questions: Contribution in IB Business Management

What is contribution analysis in IB Business Management?

Contribution analysis is an HL tool in IB Business Management (AO2, AO4) used to evaluate the profitability of individual products, projects, or divisions. It calculates the surplus remaining after variable costs are deducted from revenue - the contribution - and examines how this covers fixed costs and generates profit. Its three main applications in the IB syllabus are make or buy analysis, contribution costing, and absorption costing.

What is the difference between contribution costing and absorption costing?

Contribution costing allocates only direct (variable) costs to each product, producing a contribution figure. It is used for short-term decisions. Absorption costing goes further by also allocating indirect (fixed) costs, producing a profit figure for each product. It is used for long-term strategic decisions. The key limitation of absorption costing is that the allocation of indirect costs is subjective - different allocation methods produce different profit figures for the same product.

How do you calculate contribution per unit in IB Business Management?

Contribution per unit = Selling Price (P) − Average Variable Cost (AVC). For example, if a product sells for $30 and its variable cost is $18, contribution per unit = $30 − $18 = $12. This $12 contributes towards covering the firm's fixed costs. Once fixed costs are covered, each additional unit sold generates $12 of profit. The break-even point in units = Fixed Costs ÷ Contribution per unit.

What is make or buy analysis in IB Business Management?

Make or buy analysis is a decision-making tool that determines whether a business should produce a component or product in-house (make) or purchase it from an external supplier (buy). The quantitative comparison is between the cost to make (CTM) and the cost to buy (CTB). If CTB is lower, there is a financial case for outsourcing. However, managers must also consider qualitative factors including quality, lead times, intellectual property protection, and supplier reliability before making a final decision.

What are the limitations of absorption costing as a business tool?

The main limitation of absorption costing is that the allocation of indirect costs is subjective. Different allocation methods - for example, equal split versus proportional allocation by revenue - produce different profit figures for the same product. A manager using equal allocation might conclude that a low-revenue product is unprofitable and discontinue it, while proportional allocation would show the same product generating a positive profit. This means absorption costing results must be interpreted with caution, and businesses should apply their chosen method consistently across periods for valid comparisons.

Explore IB Business Management And Contribution

IB Business Management Main Hub your daily IB Business Management resource

IB Business Management Contribution in the Business Management Toolkit

IB Business Management Paper 1 Exam Review Hub find Contribution exam questions in Paper 1

IB Business Management Paper 2 Exam Review Hub study Contribution exam questions in Paper 2

IB Business Management Paper 3 Exam Review Hub explore Contribution exam questions in Paper 3

IB Business Management Activity Book: Explore and practice The Business Management Toolkit including Contribution, Unit 1 Swot Analysis, Unit 2 Ansoff Matrix, Unit 3 Steeple Analysis, Unit 4 Boston Consulting Group (BCG) Matrix, Unit 5 Business Plan, Unit 6 Decision Trees, Unit 7 Descriptive Statistics, Unit 8 Circular Business Models, Unit 9 Gantt Charts (HL only), Unit 10 Porter’s Generic Strategies (HL only), Unit 11 Hofstede’s cultural dimensions (HL only), Unit 12 Force Field Analysis (HL only), Unit 13 Critical Path Analysis (HL only), Unit 14 Contribution (HL only), Unit 15 Simple Linear Regression (HL only) activities, exam questions, case studies, IB Standard model answers and IB marking schemes.

Read Next: IB Business Management Toolkit Simple Linear Regression HL

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form