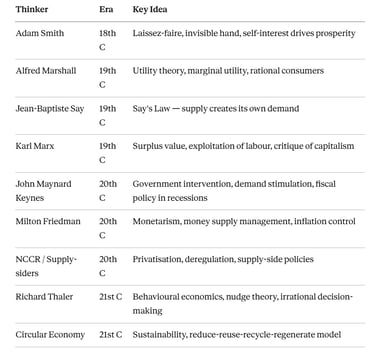

IB Economics Adam Smith & Economic Thought

A complete guide to economic thought for IB Economics - covering Adam Smith, Keynes, Friedman, Thaler, and the circular economy, with real-world examples and exam-ready theory.

IB ECONOMICS HLIB ECONOMICSIB ECONOMICS SLIB ECONOMICS INTRODUCTION

Lawrence Robert

5/15/202516 min read

A Brief History of Economic Thought - From Adam Smith to Behavioural Economics

Target Question:

What are the main schools of economic thought in IB Economics?

The Guy Who Started It All (In a Café, Apparently)

Edinburgh, 1759. A Scottish philosopher is sitting in a coffee house, watching people debate, trade, argue, and buy things. He's not a government minister. He's not a banker. He's just a bloke who's genuinely fascinated by why people make the economic choices they make - and whether society would be better off if the government just… got out of the way.

His name was Adam Smith. And the ideas he'd go on to write down would eventually change the world.

But economics as a subject has changed a lot since 1776. It has evolved. It has got some things badly wrong over the years, corrected the course, and is still evolving right now - in university lecture halls, in government policy papers, in research papers and yes, even on the apps on your phone.

That evolution - the history of economic thought - is what this entry is all about. From Smith's invisible hand to Richard Thaler's nudge, from Karl Marx's critique of capitalism to the circular economy of 2025, we're going to trace how economists have tried to answer the same fundamental question across three centuries: how do we make sense of the economic world?

What Is "Economic Thought"?

IB Economics definition - Economic thought:

Economic thought refers to the historical account of the different economic ideas, beliefs, and principles that have dominated the study of economics as a social science.

The key word here is historical. Economic ideas didn't arrive in their final version - they developed in response to what was happening in the real world. Factories were built. Empires expanded. Depressions hit. Wars broke out. Pandemics spread. And each time the world threw something new at economists, their theories either held up, collapsed, or had to be rethought again from scratch.

Economic hypotheses, models, and theories have evolved significantly over time, reflecting the changing ideas, beliefs, and principles that respond to real-world developments.

Ready? Let's start in the 18th century.

The 18th Century - Adam Smith and the Birth of Free Markets

The Economics Legend

In 1776 - the same year the Americans declared independence, your history teacher probably loves this - a Scottish economist and philosopher named Adam Smith published a book called The Wealth of Nations. Later it would become one of the most influential texts ever written.

Adam Smith (1723–1790) established the principles of free market economics in his 1776 book, The Wealth of Nations, advocating for minimal government intervention and allowing natural market forces to operate freely.

Smith was reacting against the dominant economic thinking of his era: mercantilism. Mercantilists believed that a nation's wealth depended on accumulating gold, silver, and limited resources, and that the government needed tight control over all economic activity to achieve this. This was the economic equivalent of hoarding valuable resources - the more you keep, the richer you are.

Smith thought this was nonsense.

Laissez-Faire and the Invisible Hand

His big idea was laissez-faire - a French phrase meaning, roughly, "let it be." Smith argued that the economy worked best when the government stepped back and let natural market forces do their thing. When individuals are free to pursue their own self-interest, and when genuine competition exists between producers, the result is economic well-being and prosperity for society as a whole.

This leads us to one of the most famous metaphors in all of economics: the invisible hand.

Smith argued that when individuals make rational decisions in their own best interest, they are guided - as if by an invisible hand - to produce outcomes that benefit society as a whole. A baker doesn't bake bread out of the goodness of their heart; they do it to make money. But in doing so, they feed people. A tech entrepreneur doesn't build an app out of altruism; they want a profit. But in doing so, they create something useful and create jobs.

IB Economics definition - The invisible hand:

The invisible hand describes how individuals pursuing self-interest are guided, as if by an unseen force, to produce outcomes that benefit society as a whole.

The invisible hand, in short, is the idea that markets coordinate economic activity without anyone being in charge. No central management needed. No government intervention required.

Today, Smith's influence is everywhere. When people argue for lower taxes, less regulation, and free trade - whether in Westminster, Washington, or wherever - they are, consciously or not, repeating those ideas Adam Smith laid out nearly 250 years ago. He is widely recognised as the founder of classical economic theory.

The 19th Century - Classical Economics Gets a Little Bit Sophisticated

Markets, Utility, and Rational Consumers

Smith's ideas took hold and inspired a whole school of thought: classical economics. The central claim was that markets are self-regulating - left to themselves, they efficiently allocate resources without needing government interference. Classical economists supported competitive markets, minimal government intervention, and international free trade.

But 19th century economists went further than Smith, adding additional finesse. Two of the biggest additions were utility theory and marginal utility.

Utility Theory - Alfred Marshall

IB Economics definition - Utility:

Utility is the degree of satisfaction gained from consuming a good or service; marginal utility is the additional satisfaction gained from consuming one more unit.

British economist Alfred Marshall (1842–1924) - one of the great architects of classical microeconomics - believed that rational consumers act to maximise their personal utility. That is, they make purchasing decisions designed to obtain the greatest possible satisfaction from their limited income.

You're at a summer music festival. You're starving. You pay £8 for a burger and it's the best thing you've ever tasted. Complete satisfaction. Utility: maximum. You eat a second burger. Still pretty good. Third burger? You're a bit full now. Fourth? You're starting to feel sick. The satisfaction from each additional burger is declining with every bite.

That is the law of diminishing marginal utility

IB Economics definition - Law of diminishing marginal utility:

The law of diminishing marginal utility states that as consumption increases, the additional satisfaction gained from each extra unit declines.

Marginal utility refers to the additional satisfaction gained from consuming one more unit of a product. And the law says: as consumption increases, marginal utility falls. Each extra unit gives you a little less pleasure than the one before.

This simple concept is behind an enormous amount of modern economic theory - including how we explain consumer behaviour, demand curves, and pricing strategies. Not bad at all for something you can test with a bag of crisps.

Say's Law - Supply Creates Its Own Demand

French classical economist Jean-Baptiste Say (1767–1832) contributed one of the most debated ideas in economic history.

IB Economics definition - Say's Law states:

Supply creates its own demand - the act of production generates the income needed to purchase goods.

The logic goes like this. In order to buy something, you first have to earn income. To earn income, you have to produce something - a good, a service, your labour. So production is the foundation of consumption. The act of making things generates the income needed to buy things.

The implications? A nation's long-run prosperity comes from its productive capacity. Don't focus on stimulating consumption - focus on producing more. Free markets, competition, and open international trade are therefore the engines of growth.

Say's Law strongly influenced supply-side economic thinking in the 20th century - we'll come back to that.

Karl Marx - The Radical Challenger

Not everyone in the 19th century was in support of capitalism.

Karl Marx (1818–1883), German philosopher and sociologist, looked at the industrialising economy around him and saw something very different from Adam Smith's invisible hand. He saw exploitation.

Marx introduced the concept of surplus value: the idea that workers produce more value than they are paid for, and the difference is extracted by the capitalist class as profit. In other words, the wealth accumulating at the top of society came directly from the labour of workers at the bottom - and the system was structurally designed to keep it that way.

Marxism prioritises the needs and values of the majority - the workers - rather than the interests of a privileged few. He called for radical change: collective ownership of the means of production, the abolition of private property, and a society organised around the principle of "from each according to their ability, to each according to their needs."

Marx's ideas went on to inspire communism, which spread across Eastern Europe and parts of Asia in the first half of the 20th century. Whatever you think of his conclusions, his diagnosis of inequality within capitalist systems remains one of the most powerful critiques ever written - and the debates he sparked are still live today. Just look at any conversation about wealth taxes, workers' rights, or executive pay.

The 20th Century - The Great Debates

The Great Depression and the Keynesian Revolution

In 1929 the New York Stock Exchange collapses. Banks fail across the United States and Europe. Factories close. Unemployment rockets. The global economy enters freefall - what we now call the Great Depression.

Classical economics had an answer: don't panic, let the market self-correct. Workers would accept lower wages. Businesses would adjust prices. The invisible hand would sort it out eventually.

The problem? "Eventually" was taking far too long, and millions of people were suffering in the meantime. So into this chaos stepped one of the most important economists who ever lived.

John Maynard Keynes (1883–1946)

John Maynard Keynes was a Cambridge economist with an extraordinary gift for both theory and real-world application. He looked at the Great Depression and came to the following conclusion:

The problem wasn't that markets hadn't corrected yet. The problem was a catastrophic collapse in demand. Nobody was spending. Businesses weren't investing. Governments weren't spending enough. The whole economy had come to a halt because there simply wasn't enough aggregate demand to get things moving again.

What was Keynes' solution? Government intervention. Specifically: boost government spending and cut taxes to inject demand into the economy and drag it out of depression.

Keynesian economics argues that government intervention - specifically increased spending and tax cuts - is necessary to stimulate aggregate demand and lift economies out of recession.

This was a direct challenge to Say's Law. Keynes argued that supply does not always create its own demand - you could have massive over-production and a complete absence of buyers. The Great Depression proved it.

Keynes believed that market forces alone - the invisible hand - could not revive an economy stuck in depression or trapped in long-run unemployment. Only strategic government investment could break the cycle.

Keynesian ideas have been dusted off and implemented in almost every major economic crisis ever since. When the 2008 global financial crisis hit, governments across the UK, US, and Europe launched huge fiscal stimulus programmes - tax cuts, spending increases, bank bailouts - straight from the Keynesian playbook. When COVID-19 arrived in 2020, the UK government rolled out furlough schemes, business grants, and unprecedented borrowing to keep the economy from collapsing. Again: this is Keynes.

The man died in 1946. His ideas are still running the show in 2025.

Monetarism and Milton Friedman (1912–2006)

By the 1970s, Keynesian economics was facing a new challenge. Inflation - rising prices - was becoming a serious problem in both the US and UK, partly driven by oil price shocks and excessive government spending. And the Keynesian toolkit didn't have a great answer for it.

Milton Friedman and monetarism.

Monetarism, associated with Milton Friedman, holds that poor management of the money supply is the primary cause of macroeconomic problems such as inflation.

Friedman, who won the Nobel Prize in Economics in 1976, argued that the primary cause of macroeconomic problems - particularly inflation - was poor management of the money supply. If the government printed too much money, inflation would follow. Full stop.

His prescription was straightforward: control the money supply through monetary policy (principally interest rates), keep inflation low and stable, and let the market take care of the rest. Government should stop trying to encourage the economy through spending and taxation - it would only make things worse.

Does it sound familiar to you? It should. When the UK and European Central Bank hiked interest rates sharply between 2022 and 2024 in response to surging inflation following the COVID-19 pandemic and the Ukraine war energy crisis, they were following a fundamentally monetarist logic. Control money. Control inflation. Trust the market.

Friedman's other famous line - "There's no such thing as a free lunch" - you'll recognise from our previous entry on opportunity cost.

Supply-Side Economics and the New Classical Counter-Revolution

In the 1980s, a new force swept through economic policy. On both sides of the Atlantic, right-leaning governments - led by Margaret Thatcher in the UK and Ronald Reagan in the US - embraced what became known as supply-side economics, driven by the New Classical Counter-Revolution (NCCR).

The NCCR was, in many ways, a return to Smith and Say: the problem with modern economies wasn't weak demand. It was an inefficient, over-regulated, over-taxed, bloated supply side. What was the solution to this?

Privatise state-owned enterprises (in the UK, British Telecom, British Gas, British Airways - all sold off)

Deregulate markets to stimulate competition

Cut taxes to incentivise work, investment, and enterprise

Withdraw government regulation from markets wherever possible

These policies drew directly from Say's Law: boost productive capacity, encourage private enterprise, and growth will follow. Supply-side economists weren't interested in stimulating demand - they wanted to unleash supply.

IB Economics - Syllabus and Programme Full Guide →

The 21st Century - Behavioural Economics and the Circular Economy

Are Humans Really Rational?

Classical and neoclassical economics was built on a mistaken assumption: that people are rational. They weigh up costs and benefits, process all available information, make optimal decisions, and act consistently in their own best interests.

Anyone who has ever bought something they didn't need out of panic or boredom, stayed in a Apple store queue for three hours because leaving felt like a waste, or kept a gym membership for six months without going - raise your hand.

We are not, it turns out, reliably rational. And that's where behavioural economics comes in.

Behavioural economics sits at the fascinating crossroads of economics, psychology, and marketing. Unlike traditional economics, it acknowledges that emotions, social factors, cognitive biases, and irrational tendencies shape our economic decisions far more than classical theory ever admitted.

IB Economics definition - Behavioural economics:

Behavioural economics combines economics and psychology to explain how irrational behaviour and cognitive biases influence economic decision-making.

Richard Thaler and the Nudge

American economist Richard Thaler - awarded the Nobel Prize in Economic Sciences in 2017 - is the great leader of behavioural economics. Together with legal scholar Cass Sunstein wrote in their 2008 book Nudge that you don't need to force people into better decisions or incentivise them with financial rewards. You just need to gently architect the choices in front of them.

IB Economics definition - Nudge:

A nudge is any gentle change in the decision-making environment that steers people toward better choices without restricting their freedom to choose otherwise.

Typical nudges in action:

Organ donation opt-out systems: Instead of asking people to actively sign up to donate organs (opt-in), some countries switched to an opt-out system - you're automatically a donor unless you actively decline. The UK introduced this change in England in 2020. Donor registration rates shot up. Human behaviour hadn't changed. The default option had.

Pension auto-enrolment: Thaler co-designed the "Save More Tomorrow" programme, where employees are automatically enrolled into workplace pension schemes unless they opt out. In the UK, auto-enrolment has brought millions of people who never actively chose to save into pension schemes. Again - same people, a different default option bringing different outcomes.

School canteen design: Putting fruit at eye level and placing crisps on the bottom shelf. Nobody's banned anything. Nobody's been fined. But kids eat more fruit. That's certainly a nudge.

In 2010, David Cameron's UK government set up what became known informally as the Nudge Unit - formally, the Behavioural Insights Team - to embed these ideas into government policy. It was the first government unit of its kind in the world, and since then over 200 similar nudge units have been established in governments worldwide.

Thaler's work underlines something important: we don't always act in ways that benefit us. Often, we lack the time, information, or cognitive bandwidth to make the best decisions. Behavioural economics doesn't just point this out - it uses the insight and the information to design better systems.

The Circular Economy - Economics Meets the Planet

Can We Carry On Like This?

Every smartphone that's ever been made required lithium, cobalt, gold, and rare earth metals extracted from the ground. Most smartphones end up in a drawer, then a landfill, within two to three years. The metals? Gone. The resources? Extracted, used briefly, and then discarded.

This is the linear economy: take → make → dispose. And it's increasingly obvious that a planet with finite resources cannot sustain an economy built entirely on extraction, use, and waste.

Which is where the circular economy comes in.

What Is a Circular Economy?

IB Economics definition - Circular economy:

A circular economy creates a system where raw materials, components, and resources are used sustainably - designed to be recycled, reused, and regenerated rather than discarded.

It represents a shift towards green and renewable energy sources, and a manufacturing model built around keeping materials in circulation for as long as it is possible.

Instead of take → make → dispose, think: reduce → reuse → recycle → regenerate.

IB Economics Real-life examples are coming our way thick and fast:

The European Union's Right to Repair Directive (entered into force July 2024) now gives consumers the legal right to have their goods repaired rather than replaced. Manufacturers can no longer design products to be deliberately unrepairable - a significant step toward circular thinking at a legal level.

The EU's Packaging and Packaging Waste Regulation (PPWR) entered into force in February 2025, targeting single-use plastics and pushing manufacturers toward recyclable, reusable packaging across all member states.

In the UK, the introduction of a Recyclability Assessment Methodology will see packaging classified as red, amber, or green according to its recyclability - bringing transparency to what actually happens to the packaging you put in your recycling bin.

At the 2025 EU Green Week conference in Brussels, the United Nations highlighted how circular economy approaches - from sustainable groundwater management in Croatia to agricultural resilience in Scotland - are functioning as real-world laboratories for a more sustainable economic model.

IB Economics Summary

The circular economy links directly to two of the IB's nine central concepts: sustainability and interdependence.

Sustainability means ensuring that today's economic activity doesn't compromise the resources available to future generations. A linear economy that mines, produces, and discards is fundamentally unsustainable - it draws down finite resources to satisfy current demand while leaving future generations with less.

Interdependence reminds us that the economy, society, and the environment are deeply interconnected. Deforestation doesn't just destroy trees - it disrupts rainfall, collapses ecosystems, destroys agricultural land, and undermines economic development. The circular economy is, in basically, a recognition that you cannot sustainably separate economic thinking from environmental reality.

A Timeline of Ideas

18th century → Adam Smith argues for free markets, minimal government, and the self-regulating power of the invisible hand. Classical economics is born.

19th century → Classical economics is refined. Utility theory and marginal utility explain consumer behaviour. Say's Law argues supply creates demand. Marx challenges everything, highlighting exploitation and inequality within capitalism.

Early 20th century → The Great Depression destroys confidence in self-regulating markets. Keynes argues for government intervention to stimulate demand. The invisible hand gets a helping hand.

Mid-late 20th century → Friedman and monetarism push back against Keynesian demand management. Control the money supply; control inflation. Supply-side economics of the 1980s draws on Say's Law and classical ideas, privatising and deregulating at scale.

21st century → Behavioural economics acknowledges human irrationality and uses nudges to improve outcomes. The circular economy reframes growth and production around sustainability and resource efficiency.

The story isn't over. Economics keeps evolving...

Key Thinkers and Concepts:

Key Definitions

Economic thought: A historical account of the different economic ideas, beliefs, and principles that have shaped the study of economics as a social science.

Laissez-faire: An approach to economics advocating minimal government intervention, allowing market forces to operate freely.

The invisible hand: Adam Smith's metaphor for the self-regulating nature of markets - individuals pursuing self-interest inadvertently benefit society.

Utility: The degree of satisfaction gained from consuming a good or service.

Marginal utility: The additional satisfaction gained from consuming one more unit of a product.

Say's Law: The principle that supply creates its own demand - the act of production generates the income needed to purchase output.

Keynesian economics: The school of thought arguing that government intervention, particularly increased spending and tax cuts, is necessary to stimulate demand and lift economies out of recession.

Monetarism: The school of thought arguing that controlling the money supply is the primary tool for managing inflation and achieving long-run economic stability.

Behavioural economics: A field combining economics and psychology to understand how irrational behaviour and cognitive biases influence economic decision-making.

Nudge: A gentle intervention that steers people toward better choices without restricting their freedom to choose differently.

Circular economy: An economic model designed to eliminate waste by keeping materials in use through recycling, reuse, and regeneration.

IB Economics Diagrams Programme, What's included:

200+ exam-ready diagrams covering the entire IB Economics syllabus

Video for every diagram showing you exactly how each model looks

Image version perfect for modelling diagrams in you essays, presentations, and your IA

Detailed written explanations of the IB Economics theory behind each diagram

Both SL and HL IB Economics diagrams clearly labelled and organised by topic

Real IB Economics exam application showing how to use diagrams effectively in Paper 1 and Paper 2

Frequently Asked Questions: Economic Thought and Behavioural Economics (IB Economics)

Q1: Who is considered the founder of classical economics? Adam Smith (1723–1790) is widely regarded as the founder of classical economic theory. His 1776 book The Wealth of Nations introduced the principles of laissez-faire economics, the invisible hand, and free market thinking that shaped economic thought through the 19th century and beyond.

Q2: What is the key difference between Keynesian economics and monetarism? Keynesian economics argues that governments should actively manage aggregate demand - through increased spending and tax cuts - to stabilise the economy during recessions. Monetarism, associated with Milton Friedman, argues instead that controlling the money supply is the key to economic stability, and that excessive government intervention tends to make things worse. Both schools have been applied in real-world policy: Keynesian logic underpinned COVID-era stimulus packages, while monetarist logic drove the interest rate hikes used to tackle inflation in 2022–2024.

Q3: What is Say's Law and why is it controversial? Say's Law, proposed by Jean-Baptiste Say, states that supply creates its own demand - in other words, the act of producing goods generates the income needed to buy them. It became controversial when Keynes argued it was flatly wrong: the Great Depression showed that economies could produce far more than consumers were willing or able to buy. The debate between Say and Keynes essentially defines the tension between classical and Keynesian economics.

Q4: What is behavioural economics and how is it used in government policy? Behavioural economics is the study of how psychological factors, cognitive biases, and emotions influence economic decision-making - challenging the classical assumption that people always act rationally. Richard Thaler's nudge theory applies these insights to policy design: rather than forcing behaviour change, governments restructure choices to make better decisions the path of least resistance. Real examples include the UK's organ donation opt-out system (introduced 2020) and workplace pension auto-enrolment.

Q5: What is a circular economy and how does it relate to economics? A circular economy is an economic model that replaces the traditional linear "take-make-dispose" approach with a system of reducing, reusing, recycling, and regenerating resources. It connects to the IB Economics concepts of sustainability (meeting today's needs without harming future generations) and interdependence (recognising that economic activity, society, and the environment are deeply connected). Real-world examples include the EU's Right to Repair Directive (2024) and the EU Packaging and Packaging Waste Regulation (2025).

Stay well,

Related Topics:

IB Economics your IB Economics daily guide

IB Economics Introduction to Economics access Economic Thought content as well as the rest of module 1

IB Economics Scarcity for expanding basic economics concepts, scarcity and consumer choice

IB Economics Diagrams Check Unit 2 for All The Circular Flow of Income, Unit 1 for All PPC / PPF and Unit 3 for the Circular Economy diagrams with explanations

IB Economics Opportunity Cost for covering and revising opportunity cost theory, the reference is Milton Freedman's quote "there is no such thing as a free lunch"

IB Economics Activity book Module 1 Introduction to Economics Units 1.2 For the approaches of economists (Economic thought), unit 1.4 for The Circular Flow of Income and unit 1.3 for production possibilities PPC or PPF exam practice, activities, model answers and IB Economics Marking schemes

IB Economics Supply and IB Economics Demand Pages to elaborate on "the theory of supply and demand" →

IB Economics Paper 1 as basic economics concepts and Economic Thought may appear in this IB Economics exam paper

IB Economics Government Intervention for content that helps you continue the debate: should the government intervene in the economy or should it leave it alone?

IB Economics Aggregate Demand and IB Economics Aggregate supply for extended information on the "furlough payments... COVID-19" →

IB economics Calculations Book make sure you check unit 1 Introduction to economics for Economic Thought and basic economics calculations exercises, IB model answers, and IB marking schemes

IB Economics Keynesian versus Monetarist this content will help you get familiar with both, Keynes and monetarists ideas that will become very useful in the last part of your IB Economics course

Read Next: IB Economics Demand

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form