IB Economics Balance of Payments (HL)

Master Advanced concepts of Balance of Payments with this friendly guide to deficits, surpluses, and exchange rates. Essential for IB Economics HL students!

IB ECONOMICS HLIB ECONOMICSIB ECONOMICS THE GLOBAL ECONOMY / INTERNATIONAL TRADE

Lawrence Robert

5/4/202513 min read

Exchange Rates, Deficits, and the J-Curve

Target Question:

What is the Marshall-Lerner condition and the J-curve effect in IB Economics?

The Flatmate Who Always Owes

Let's imagine for a second that you've got a flatmate - let's call her Bex. Bex earns decent money, but she spends more than she earns. Every single month. Without fail. She buys more than she sells on her online shop. She's always borrowing a tenner here, a twenty there. She's running what economists would call a persistent deficit.

For a while, it's fine. People lend her money. Her parents occasionally bail her out. The other day she sold something valuable from her room. But eventually, people start wondering: can Bex actually pay this back? Her credit rating - unofficially, her reputation - starts to suffer. The flatmates who used to lend freely start hesitating. The bank starts charging her more interest for her overdraft.

This is a nice introduction to today's topic, the persistent current account deficit - one of the most important and most examined topics within the HL IB Economics syllabus.

We will talk about how exchange rates and the current account influence each other, what happens when a deficit runs for years, how governments try to fix it, and the logic behind the Marshall-Lerner condition and the J-curve effect.

Part One: Exchange Rates and the Current Account - A Two-Way Relationship

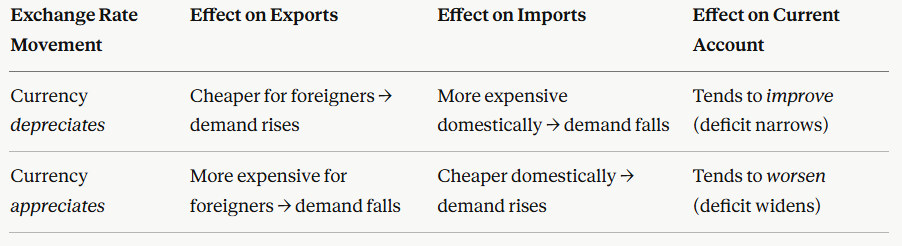

How Trade Affects Currencies

You already know that when a European consumer buys an American product - say, a pair of Air Jordans - they need US dollars to pay for it. That means they must sell euros and buy dollars on the foreign exchange market. This:

Increases demand for US dollars → dollar appreciates (credit to the US economy)

Increases supply of euros → euro depreciates (debit to the European economy)

In a freely floating exchange rate system, this process is continuous and automatic. If the US runs a current account surplus (Americans sell more to Europe than they buy), demand for dollars rises, the dollar appreciates, US exports become more expensive, and Europeans buy less of them. Equilibrium is theoretically restored over time.

The key relationship is this one: the value of the domestic currency and the current account balance are inversely related.

For access to all IB Economics exam practice questions, model answers, IB Economics complete diagrams together with full explanations, and detailed assessment criteria, explore the Complete IB Economics Course

IB Economics Real-life Example:

The post-Brexit pound is a decent example here. When sterling fell sharply after the 2016 referendum, UK exports became cheaper in theory - but the improvement in the current account took time, and was incomplete, partly because of other structural issues. During 2008-09, the depreciation of the pound didn't affect the UK's current account deficit meaningfully, largely because of the slow global growth - there was simply little foreign demand for UK exports despite the fall in price.

In a fixed exchange rate system, the automatic adjustment mechanism is not in place. Meaning that the only way to get the same effect is if the government deliberately devalues the currency - an interventionist policy decision, not a market outcome.

The Financial Account and Exchange Rates

It's not just trade that moves currencies. Investment flows do too - and this is where the financial account connects to exchange rates.

When foreign investors want to put money into a country - buying its bonds, its shares, or setting up factories - they need to buy the domestic currency first. This increased demand pushes the currency's value up.

When those investments eventually generate returns - dividends from stocks, interest from bonds - the foreign investor converts those earnings back into their own currency. That means selling the domestic currency, increasing its supply, and putting downward pressure on the exchange rate.

So: financial account inflows → currency appreciates.

But the dividend/interest payments flowing back out later → currency depreciates. It's a cycle that keeps economists very busy.

Part Two: What Happens When a Deficit Doesn't Go Away

A current account deficit for one year? Fine. Manageable. Happens to most countries. But a persistent deficit - one that grinds on year after year - generates a combination of significant problems. Here are the seven key implications from your IB Economics syllabus:

1. Exchange Rate Pressure

Running a persistent deficit means you're constantly selling domestic currency to pay for imports. That excess supply of domestic currency pushes its value down. For countries that depend on imported essentials - oil, food, raw materials - a weaker currency is extremely painful. Everything imported gets more expensive, putting pressure on both, households and businesses. Costs rise, output potentially falls, and employment suffers.

IB Economics Real-life Example:

In 2008, some Eurozone economies had current account deficits exceeding 10% of GDP - particularly Portugal, Greece, and Spain - which was a sign of an unbalanced economy and a fundamental lack of competitiveness. Crucially, those countries couldn't even let their currencies depreciate to self-correct, because they were locked into the euro. Which is why the fallout was so severe.

2. Interest Rate Pressure

A weakening exchange rate can force a government's hand on interest rates. Raise rates → attract foreign capital → prop up the currency. But higher interest rates mean more expensive borrowing for households and firms. Aggregate demand falls. If rates stay high long enough, you're looking at a recession and rising unemployment. The deficit cure becomes its own disease.

3. Foreign Ownership of Domestic Assets

To finance the deficit, a country typically runs a financial account surplus - attracting FDI and portfolio investment. That's fine up to a point. But it means foreign companies and investors steadily accumulate ownership of domestic businesses, property, and government debt.

IB Economics Real-life Example:

The UK is a relevant case here: the UK's net international investment position was negative £271.4 billion in 2024 - the rest of the world owns significantly more UK assets than UK investors own abroad. That level of foreign ownership can leave the domestic economy strategically vulnerable, particularly if overseas investors start making decisions that prioritise their own interests over the host economy's.

4. Debt Accumulation

If a country can't attract enough investment to cover its deficit, it borrows. That borrowing enters the financial account, but it also means rising national debt, growing interest repayments, and reduced fiscal space for public spending. Eventually the debt itself becomes the problem.

5. Credit Rating Deterioration

A persistent deficit signals potential economic fragility to the international credit agencies - Moody's, S&P, Fitch. A downgraded credit rating means the country is seen as a higher risk, so lenders charge higher interest rates. That makes borrowing more expensive, which discourages investment and growth. It's a confidence spiral that's genuinely hard to reverse.

6. Demand Management Complications

High domestic spending is often the cause of a current account deficit - people and businesses buying imports enthusiastically. Contractionary demand management (higher taxes, spending cuts) can reduce import demand. But it also slows the whole economy. You fix the deficit by suppressing growth. In reality, it's a uncomfortable trade-off.

7. Long-Run Growth Consequences

Combine reduced aggregate demand, weaker confidence, higher debt servicing costs, and a deteriorating credit rating, and you end up with an economy that struggles to grow. Investment dries up. Consumers cut back. The deficit might narrow - but for the wrong reasons.

Every episode of Pint-Sized links back to what matters most for your IB Economics course:

Understanding key IB Economics concepts

Applying them in real-world IB Economics contexts

Building IB Economics course confidence without drowning in dry theory.

Subscribe for free to exclusive episodes designed to boost your IB Economics grades and confidence

Part Three: How Governments Try to Fix It

There are three families of policy tools, and each comes with trade-offs.

1. Expenditure-Switching Policies

IB Economics definition - Expenditure-Switching Policies:

Government measures designed to shift domestic and overseas spending away from imports and toward domestically produced goods and services, including export subsidies, tariffs, quotas, and currency devaluation.

The goal: get domestic consumers and overseas buyers to switch their spending - away from foreign goods and towards domestically produced ones.

a) Export Promotion (subsidies) Government subsidies make domestic industries more competitive internationally. More exports = more credit items = narrowing deficit. What would be the issue here? It costs money - public funds with opportunity costs attached - and can trigger accusations of unfair competition from trading partners.

b) Trade Protection (tariffs and quotas) Make imports more expensive or restrict their quantity, and consumers might switch to domestic alternatives. But trade protection is a sharp instrument. It can shield inefficient domestic industries from the competitive pressure that would otherwise make them improve, and also trading partners tend to retaliate - sparking trade wars that hurt everyone. The US-China tariff escalation of 2025 is a good example of how it works.

c) Currency Devaluation Governments operating a fixed exchange rate can devalue their currency deliberately - making exports cheaper and imports pricier. In a floating system, this happens automatically through depreciation. What is the main risk? A devalued/depreciated currency imports inflation. Oil, raw materials, food - all priced in foreign currencies - become more expensive. The cost of living rises. What fixes the trade balance can punish ordinary households.

2. Expenditure-Reducing Policies

IB Economics definition - Expenditure-Reducing Policies:

Contractionary demand-side policies - such as higher interest rates or tax increases - that reduce overall domestic spending, thereby lowering import demand and narrowing a current account deficit.

The goal: reduce domestic income and spending, so households and firms import less.

a) Contractionary Monetary Policy Raise interest rates. Borrowing becomes more expensive, saving becomes more attractive, spending falls - including spending on imports. But this discourages aggregate demand, and therefore, risks unemployment, and can tip the economy into recession.

b) Contractionary Fiscal Policy Tax rises and spending cuts reduce disposable income and government outlays, compressing import demand. Same problem: the medicine affects the whole economy, not just the import side of it.

3. Supply-Side Policies

The goal: make domestic industries so competitive that exports rise naturally and import substitution becomes attractive over time.

This is the most sustainable long-term approach. Invest in education, healthcare, infrastructure, and innovation - boost productivity, improve the quality of exports, reduce input costs.

IB Economics Real-life Example: Germany's model of world-class engineering education feeding directly into premium export industries (BMW, Siemens, BASF) is a great supply-side success story.

What are the restrictions? Time. Supply-side policies take years, sometimes decades, to deliver results. They're also expensive. A government facing pressure to fix the deficit now can't usually wait a decade for supply-side policies to produce results.

IB Economics - Syllabus and Programme Full Guide →

Are Any of These Actually Effective?

Expenditure-switching policies don't guarantee success, because price isn't everything. German cars sell at premium prices partly because of brand and quality - a weaker competitor currency doesn't automatically shift buyers away from a product they love. Non-price factors matter.

Expenditure-reducing policies can cause more damage than the deficit itself - recession and unemployment are high prices to pay.

Trade protection invites retaliation and reduces overall economic welfare - it's a politically tempting but at the same time, an economically costly tool.

Currency devaluation only works under a fixed exchange rate system, and even then it imports inflation.

Supply-side policies are the most sustainable but the slowest - and costly upfront.

The degree of effectiveness of these tools depends critically on the price elasticity of demand for exports and imports.

Part Four: The Marshall-Lerner Condition

A lot of my students usually have issues understanding why currency depreciation doesn't always fix a deficit. Let's try to explain it properly:

When a currency depreciates:

Exports become cheaper for foreigners

Imports become more expensive for domestic buyers

Intuition says this should improve the current account. But whether it actually does depends on how responsive buyers are to those price changes - in other words, on the price elasticity of demand (PED) for exports and imports.

IB Economics definition - The Marshall-Lerner condition:

The principle that a currency depreciation or devaluation will improve a country's current account balance only if the sum of the price elasticity of demand for exports and imports exceeds one.

PED(X) + PED(M) > 1

Suppose the UK's pound falls by 10%. Exports are now 10% cheaper. But if foreign buyers don't increase how much they buy significantly (inelastic demand), export revenue barely rises. Meanwhile, imports are 10% more expensive - but if UK consumers still need those imports (petrol, medical equipment, food), they keep buying them and spend more in total. The deficit gets worse, not better. Source visit: IB Economics Diagrams

The three scenarios:

IB Economics Diagrams Programme, What's included:

200+ exam-ready diagrams covering the entire IB Economics syllabus

Video for every diagram showing you exactly how each model looks

Image version perfect for modelling diagrams in you essays, presentations, and your IA

Detailed written explanations of the IB Economics theory behind each diagram

Both SL and HL IB Economics diagrams clearly labelled and organised by topic

Real IB Economics exam application showing how to use diagrams effectively in Paper 1 and Paper 2

Condition / Result

PED(X) + PED(M) > 1 Depreciation improves the current account

PED(X) + PED(M) = 1 Depreciation has no net effect on the current account

PED(X) + PED(M) < 1 Depreciation worsens the current account

Part Five: The J-Curve Effect

So we know depreciation only works if the Marshall-Lerner condition is satisfied. But we are also going to learn that even when it is satisfied, the improvement doesn't happen immediately thanks to the J-curve effect.

IB Economics definition - J-Curve Effect:

The phenomenon whereby a currency depreciation initially worsens a country's current account deficit before improving it, due to the time required for export and import volumes to adjust to new relative prices. The curve traces a J-shape over time.

Imagine the shape of the letter J for a sec. Initially, the curve dips down - the deficit gets worse. Then it curves back up - the deficit improves. That's the J-curve.

Why does it dip first?

In the short run, businesses and households have existing contracts. An importer who signed a six-month supply deal can't just cancel it because the exchange rate moved. Export orders take time to materialise. Operations and habits are sticky. So immediately after depreciation:

Import costs rise (currency is worth less, but people still buy the same volume)

Export revenues are slow to rise (foreign buyers haven't adjusted yet)

Result: the deficit initially widens. This is the movement from point A to point B on the J-curve diagram.

Over time - months, sometimes a couple of years - firms and households adjust. Foreign buyers switch to the now-cheaper exports. Domestic buyers find substitutes for the now-pricier imports. PED becomes more elastic with time.

Result: the deficit starts to improve. This is the movement from B to C. Source visit: IB Economics Diagrams

IB Economics Real-life Example: After the 1997 Asian financial crisis, many Asian countries saw an initial worsening of their trade balances before eventual improvement, as their currencies depreciated. The J-curve was visible in real time.

Two critical points for your exam:

The J-curve only occurs if the Marshall-Lerner condition is ultimately satisfied

An inverse J-curve works in the opposite direction - a currency revaluation or appreciation for a surplus country will initially worsen (increase) the surplus before it narrows over time

Part Six: Is a Surplus Always a Good Thing?

IB Economics definition - Persistent Current Account Surplus:

A prolonged situation where a country's export earnings exceed import spending, which can lead to currency appreciation, demand-pull inflation, export complacency, and trade tensions with deficit-running trading partners.

A persistent current account surplus isn't automatically great news. Here's why:

1. Domestic Consumption and Investment - Short vs Long Run

Yes, in the short run, a surplus boosts aggregate demand (X > M adds to AD), expands output from Y1 to Y2, and creates jobs. But the inflation that follows can deter future investment and erode competitiveness over time.

2. Currency Appreciation

A surplus means the rest of the world is buying more of your stuff than you're buying from them - higher demand for your currency pushes its value up. A stronger currency makes your exports progressively more expensive for overseas buyers. The very success of your export sector eventually undermines it.

IB Economics Real-life Example:

Germany is currently living this dynamic - Germany recorded an overall trade surplus of approximately €243 billion in 2024, but a strong euro makes its products increasingly expensive for key markets.

3. Inflation

A persistent surplus means continuously rising net exports and this drives AD upward - and this creates demand-pull inflation. Higher domestic prices gradually erode the international competitiveness that created the surplus in the first place. China is currently dealing with exactly this tension - though its managed exchange rate adds additional complexities.

4. Employment - The Zero-Sum Problem

Export-led growth creates jobs domestically. China's current account surplus reached $422 billion in 2024, with a goods trade surplus of $767.9 billion - an enormous engine of domestic employment. But one country's surplus is another country's deficit, and those deficit countries are losing output and jobs as they see China's gains. The political consequences - tariffs, trade disputes, WTO complaints - are very much the result of this.

5. Export Complacency

A country enjoying a sustained surplus can become complacent. Firms enjoying strong export revenues thanks to favourable exchange rates and strong global demand have less pressure to innovate, invest in efficiency, or develop new products. When conditions shift, and they always do - and as they did for Germany with Chinese competition eating into its European market share - those firms can find themselves suddenly exposed.

Is The Origin of the Surplus Relevant?

The answer is yes - and this is a great evaluation point. A surplus generated through genuine export competitiveness (Germany's engineering prowess, South Korea's electronics industry) is broadly positive - it reflects real productive strength. A surplus generated through trade protection measures (artificially suppressing imports) creates welfare losses for domestic consumers and efficiency losses for the economy overall. The source of the surplus determines whether it's something to celebrate or something to worry about.

Frequently Asked Questions: Balance of Payments, Exchange Rates, Deficits and The J-Curve (IB Economics)

Q1: What is the Marshall-Lerner condition in simple terms? It's the rule that explains that currency depreciation will only fix a current account deficit if buyers are responsive enough to the new prices. Specifically, the combined price elasticity of demand for exports and imports must add up to more than 1. If demand is too inelastic - people keep buying the same amount regardless of price - depreciation actually makes the deficit worse.

Q2: Why does the J-curve happen? Because in the short run, contracts, habits, and market inertia mean that export and import volumes don't change immediately after a depreciation. Import costs rise straight away (same volume, higher price), but export revenues take time to grow. So the current account initially deteriorates. Over time, as buyers adjust, the improvement kicks in - tracing the upward curve of the J.

Q3: What are the three types of policies used to correct a current account deficit? Expenditure-switching policies (redirecting spending from imports to domestic goods - via subsidies, tariffs, or currency devaluation), expenditure-reducing policies (contractionary fiscal or monetary policy to lower overall spending and import demand), and supply-side policies (long-term investment in education, infrastructure, and productivity to improve export competitiveness). None of them are guaranteed to work in isolation.

Q4: Is a current account surplus always a good thing? Not necessarily. A persistent surplus can cause currency appreciation (making exports progressively more expensive), demand-pull inflation, export sector complacency, and trade tensions with deficit-running partners. China's record $422 billion surplus in 2024 has reignited exactly those tensions with the US and EU. Whether a surplus is desirable depends significantly on where it comes from - genuine export competitiveness is healthy; trade protection-driven surpluses are less so.

Q5: What's the difference between currency depreciation and devaluation? Depreciation happens automatically in a floating exchange rate system - market forces push the currency's value down. Devaluation is a deliberate policy choice in a fixed exchange rate system - the government decides to lower the official exchange rate. Both have similar effects on exports and imports, but devaluation is a one-time policy decision rather than a market-driven movement.

Stay well,

Related Topics:

IB Economics your IB Economics daily guide

IB Economics The Global Economy access The Balance of Payments HL Section here as well as the rest of the module 4

IB Economics Activity book Module 4 The Global Economy Unit 4.8 for The Balance of Payments HL Section exam practice, activities, model answers and IB Economics Marking schemes

IB Economics Exchange Rates → prerequisite knowledge for the floating / fixed distinction

IB Economics Diagrams Check Unit 28 for All The Balance of Payments HL Section diagrams with explanations

IB Economics Paper 1 → relevant hub page for exam prep

IB Economics Monetary Policy and Interest Rates → connects to expenditure-reducing policy discussion

IB Economics Paper 2 Exam Tips → relevant hub page for exam prep

IB Economics Paper 3 → relevant hub page for exam prep

IB Economics HL your go to page for HL Economics Content

IB Economics Trade Protection - Tariffs and Quotas → relevant to expenditure-switching discussion

IB economics Calculations Book make sure you check unit 25 for The Balance of Payments HL Section calculations exercises, IB model answers, and IB marking schemes

Read Next: IB Economics Sustainable Development

© Theibtrainer.com 2012-2026. All rights reserved.

Legal

Have a Tip? Send us a tip using our anonymous form